The Death Benefit: Fiscal Fictions Part IV

The Government's Greatest Gift to the Wealthy Should Have a Name

This is the fourth essay in a series on fiscal fictions — the legal and accounting artifacts that present governance choices as economic necessities, and policy decisions as natural features of the landscape. The first three essays examined the architecture of government finance: the Social Security Trust Fund is not a savings account; the debt ceiling is a political tool, not a fiscal constraint; the government’s ability to create money is not what the standard story describes. Those essays established a pattern: what appears to be an iron law of public finance turns out, on inspection, to be a political choice dressed in the language of necessity — a choice that serves specific interests while appearing to serve everyone.

This essay turns from the architecture of government finance to the structure of taxation. The same pattern operates here. A provision that appears to be a neutral feature of the tax code — the absence of capital gains tax on inherited assets — is in fact a deliberate policy choice, worth roughly $72 billion in foregone federal revenue each year, that flows almost entirely to those who need it least. It has a name in the tax policy literature: the Angel of Death loophole. That name captures the mechanism but misses the structure. A loophole is something narrow and accidental. This is a benefit — deliberately awarded, architecturally embedded, and protected for a century by a label that has successfully named it out of existence.

The correct name is the Death Benefit.

I. The Label Does the Work

The term “death tax” is a piece of smart political framing. It implies that death triggers a new burden — that the government, at the moment of a family’s greatest loss, reaches in and takes a portion of what would otherwise pass intact to the next generation. The framing is powerful precisely because it is visceral: death as the occasion for government intrusion, the bereaved family as the victim. This framing has worked remarkably well. For decades it has suppressed public understanding of a provision that costs the Treasury roughly $72 billion annually — a provision that, properly understood, gives rather than takes.1

Under current American law, death is simply not a taxable event. It is the occasion on which the government delivers its greatest financial gift to wealthy estates: the permanent forgiveness of a lifetime of accumulated, untaxed appreciation. The correct label is not the death tax. It is the Death Benefit.

The collision with life insurance terminology is deliberate. A life insurance death benefit is a payment earned by paying premiums over a lifetime — a contracted sum, modest relative to the wealth it protects, that provides a family some security after a loss. The tax code’s Death Benefit is something else: a permanent forgiveness of capital gains that may run to millions of dollars — or, for the largest estates, to hundreds of millions or more — earned not by either paying premiums or taxes but simply by dying before selling. Both are triggered by death. Both flow to heirs. Only one has a name in public discourse. The life insurance industry named its product. The tax code’s Death Benefit has successfully avoided being named at all — and a benefit without a name is a benefit that cannot be discussed, debated, or reformed in ordinary political conversation. We are left able to talk only about the thing that is named but does not exist — the death tax — while the thing that exists but has no name remains invisible.2

The academic and professional tax policy literature uses a different term: the Angel of Death loophole. That name circulates among tax lawyers, economists, and policy analysts — those who already understand the tax code’s intricacy and are debating its reform in specialized venues. It has never entered ordinary political discourse, and not only because it is too technical. “Loophole” is the wrong word. A loophole is something narrow and accidental, the product of inattention, something that a careful lawyer might find and exploit. The Death Benefit is none of those things. It is a $72 billion annual policy choice, embedded in the Internal Revenue Code since 1921, that has survived every serious reform effort for a century. It is not a loophole. It is an architecture. Calling it a loophole understates what it is. Calling it a death tax inverts its effect. The accurate name is the one that has been successfully suppressed: it is a benefit, awarded at death, to those fortunate enough to have been able to spend a lifetime accumulating what they did not need to sell.

II. How the Mechanism Works

The Death Benefit operates through a provision called step-up in basis. Understanding it requires understanding what “basis” means — which is less technical than it sounds.

When you buy an asset — a share of stock, a piece of real estate, an interest in a business — the price you paid is your basis. When you eventually sell, you owe capital gains tax on the difference between what you received and what you paid: the gain above your basis. If you bought stock for $100,000 and sold it for $400,000, your basis is $100,000, your gain is $300,000, and you owe capital gains tax on $300,000. This is how the tax is supposed to work for everyone. You pay once, on the gain, when you realize it.

Step-up in basis changes this calculation at death. When an asset passes to an heir, the heir’s basis is not the benefactor’s cost of the asset — it is the asset’s fair market value on the date of death. The heir “steps up” to the current value. If that same stock, purchased for $100,000, is worth $400,000 when the owner dies, the heir inherits it with a basis of $400,000. If the heir sells it the next morning for $400,000, the gain is zero. The $300,000 in appreciation — the entire economic gain the asset produced during the owner’s lifetime — has permanently vanished from the tax base. It will never be taxed. Not as capital gains. Not as income. Not as anything.

Three things happen simultaneously at death: the basis resets to fair market value, the lifetime gain permanently escapes taxation, and the heir can sell immediately without owing a dollar in capital gains tax. The government asks for nothing. The appreciation disappears.

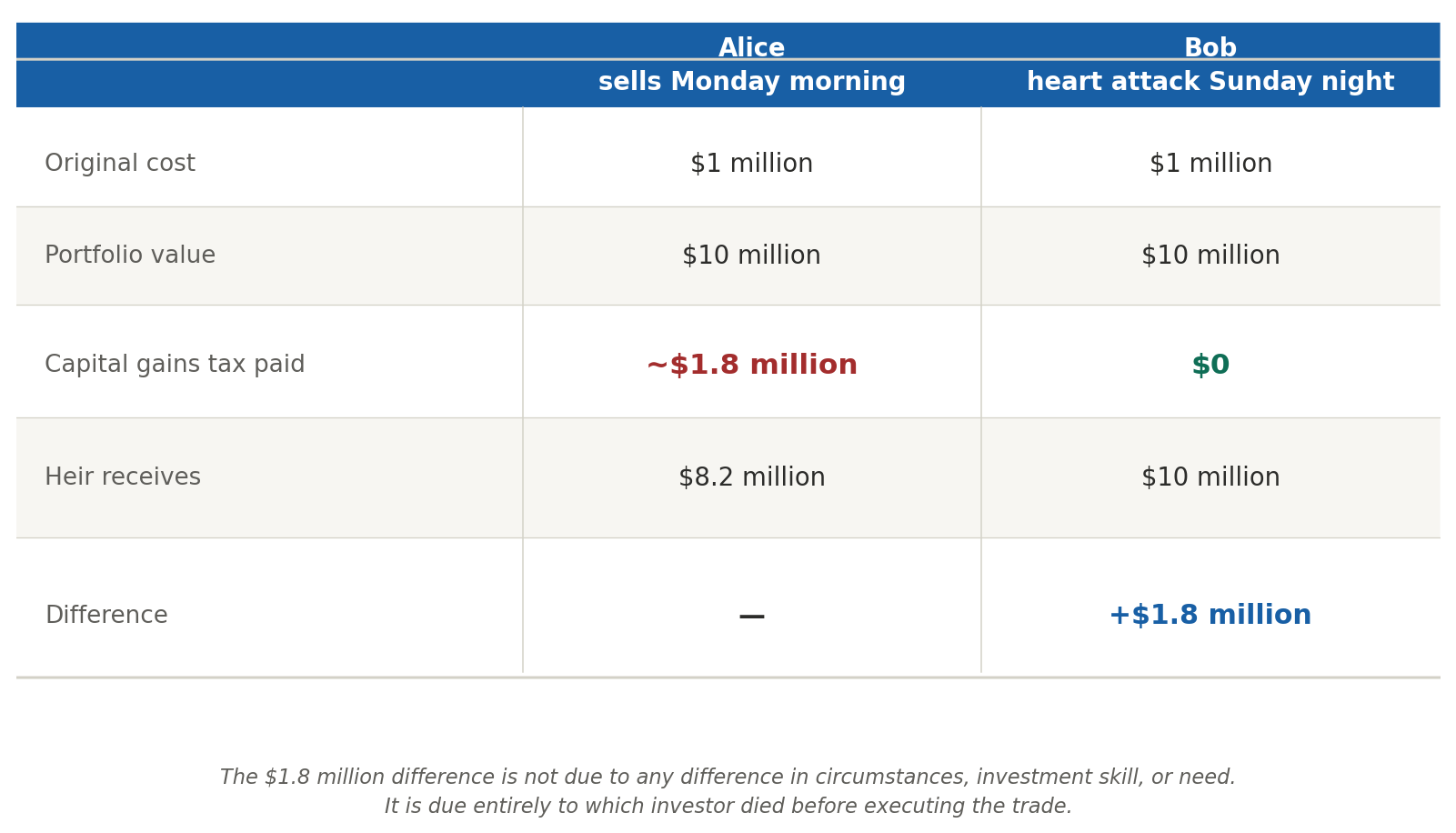

The heart attack example

Consider two investors with identical investment portfolios — each holds stock purchased years ago for $1 million, now worth $10 million. Alice sells on Monday morning. She owes capital gains tax on $9 million in appreciation — roughly $1.8 million at current rates. Her daughter inherits $8.2 million.

Bob planned to sell on Monday, but has a heart attack Sunday night, before selling. His daughter inherits the entire $10 million with a stepped-up basis of $10 million. She sells Monday morning and owes zero capital gains tax.

The $1.8 million difference between these two families was not due to any difference in their economic circumstances, their investment skill, their contribution to society, or their need. It was due entirely to which investor died before executing the trade. The tax code does not treat these families differently because their situations differ. It treats them differently because one of them died at the right moment.

For the properly positioned estate, dying is not a cost. It is a windfall.3

The history of the provision

Step-up in basis is not an ancient feature of American tax law. It was introduced in the Revenue Act of 1921 — only five years after the modern estate tax became law in 1916. Congress’s purpose was explicit and, in its original context, defensible: an asset that had just been subjected to estate tax at its full fair market value should not also face capital gains tax on the previously taxed appreciation when the heir sells. The basis was reset to fair market value to prevent double taxation. Step-up was not a gift. It was a receipt — the accounting acknowledgment that the appreciation had been taxed once, at the estate level, and should not be taxed again.

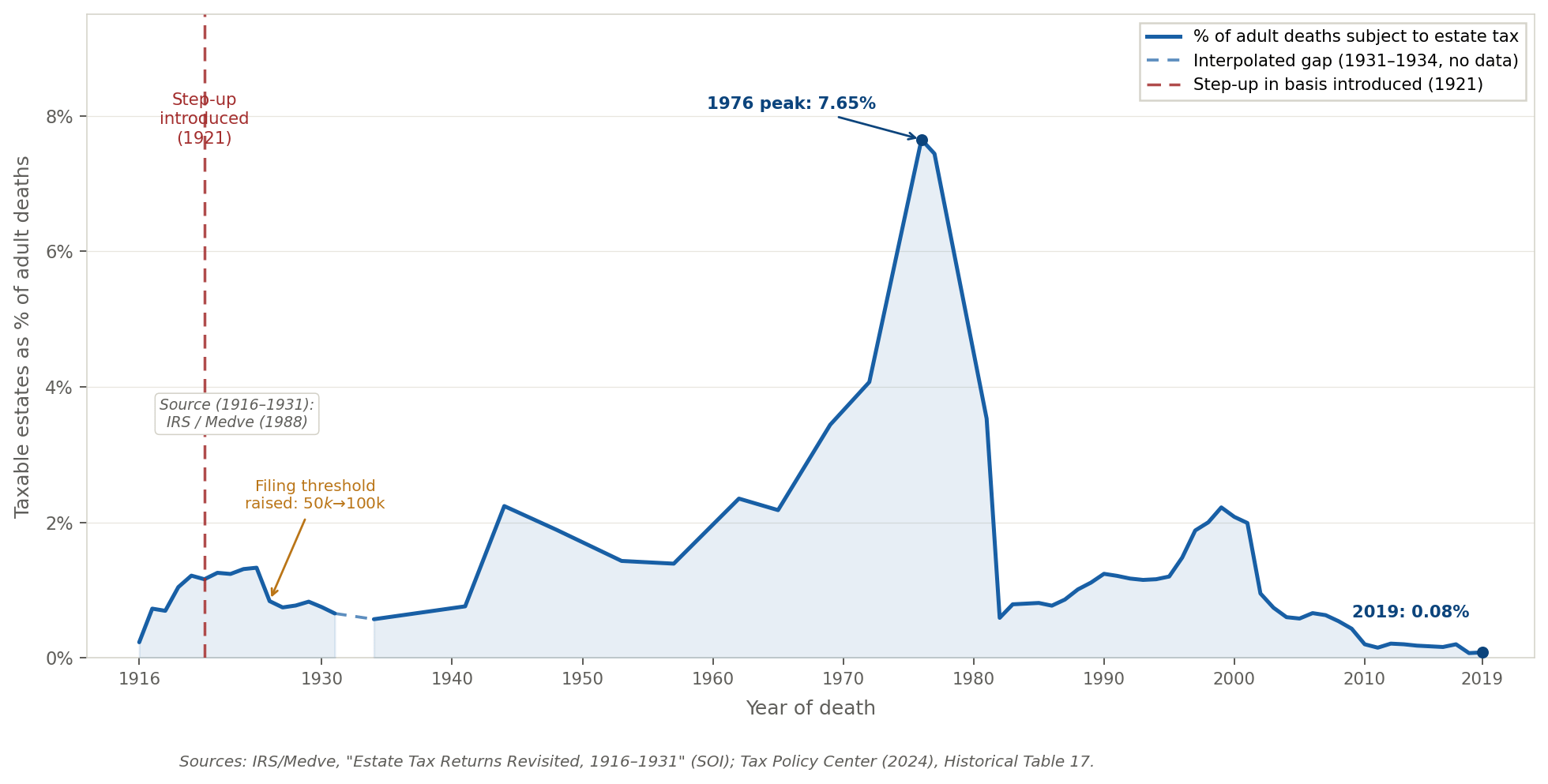

That logic was sound for any estate actually subject to estate tax — step-up prevented the appreciation from being taxed again after the estate had already paid tax on it. The problem is that step-up was written as a universal rule, applying to every estate regardless of whether estate tax was paid. In 1916, the estate tax reached 0.454% of the population — a small but real fraction of wealthy estates for whom the double-taxation concern was genuine. At its peak coverage in 1976, it applied to roughly 7% of all deaths. As long as the estate tax covered a substantial fraction of estates, the mismatch between the universal rule and the conditional rationale was modest. The subsequent decades brought a series of legislative increases to the exemption threshold: from $600,000 in the 1980s through the Bush-era escalations of the early 2000s, to the Tax Cuts and Jobs Act of 2017, which doubled the exemption to roughly $11 million per individual. That increase was originally scheduled to sunset after 2025; the One Big Beautiful Bill Act made it permanent. Today the exemption stands at $13.99 million per individual — and the estate tax reaches fewer than one estate in a thousand, 0.08% of adult deaths. The universal rule has become a near-universal gift: the original rationale applying to almost no one, the benefit flowing to almost everyone.

The provision Congress designed as a receipt for taxes paid has become, for 999 estates in a thousand, a pure tax forgiveness — the Death Benefit — awarded where no estate tax was paid and no complementary tax exists to justify it.

Preventing double taxation has become no taxation.4

The dynastic engine

For most estates, the Death Benefit is a one-time, windfall event: a lifetime of appreciated gains forgiven at a single death, the heir receiving a fresh basis, the cycle ending there. But for estates large enough to sustain a specific financial strategy, the Death Benefit becomes something more: the mechanism that powers a dynastic engine that can run without interruption across generations.

The strategy is straightforward, and it requires no offshore accounts, no complex trust structures, no aggressive legal position. It requires only a portfolio large enough to sustain low-cost collateralized borrowing, and an appreciation rate that exceeds the cost of borrowing against it.

A family holding a large diversified portfolio — equities, real estate, private investments — borrows against those holdings rather than selling them. The borrowed money funds consumption. Interest on the loans is serviced from the portfolio’s dividend and interest income, from modest additional borrowing against growing collateral, or from minimal asset sales. Lenders are comfortable with this arrangement because the portfolio’s appreciation rate keeps the loan-to-value ratio well within safe limits regardless of how long the loan runs — the collateral grows faster than the debt. The portfolio continues to appreciate. No large realization event is ever required.

At death, the accumulated appreciation is permanently forgiven through step-up. The portfolio passes to the next generation with a fresh basis — every dollar of lifetime appreciation extinguished from the tax base. The heirs retire any outstanding loans from sales of stepped-up assets, paying zero capital gains tax on those sales because the basis equals the sale price. They inherit the remaining portfolio at its new, reset basis and restart the cycle.

The government is not entirely shut out. It collects income tax on the dividends and interest the portfolio generates — the modest cash yield that even a growth-oriented family cannot fully eliminate. What it will not collect is tax on the appreciation, typically the larger component of total return by a substantial margin. For a portfolio constructed to minimize yield — low-dividend equities, real estate held for appreciation rather than income — the taxable fraction of total economic return may be a small portion of actual wealth accumulation. The tax code taxes the trickle. The flood is tax free.

This is the complete borrow-spend-die strategy: borrow against appreciating assets, service the interest from portfolio income, retire the principal at death from stepped-up sales that generate no taxable gain, and repeat across generations. It is not exotic. It is the straightforward rational response to the incentive structure the Death Benefit creates. The strategy has a simpler name in the parlance of old money: never touch the principal. Wealthy families have passed this maxim down for generations — live off the income, borrow against the growth if needed, and preserve the corpus intact for your heirs. The Death Benefit is what transforms that maxim from prudent advice into a tax-optimized dynasty engine: without step-up, the preserved principal would eventually face capital gains tax; with it, the corpus resets at each generational transfer, permanently untaxed, and the next generation begins the cycle anew with a clean slate. The tax code has made dying, for those with enough wealth to hold until it happens, among the most tax-advantaged wealth-transfer mechanisms available under American law.5

Step-up and the dynamics of concentration

Piketty’s central observation in Capital in the Twenty-First Century is that when the return on capital persistently exceeds the economy’s growth rate — r > g — wealth concentration compounds across generations without self-correcting. Dynastic strategies operate within this environment and amplify it in a specific way. A large diversified portfolio tends to earn above-average returns — scale provides access to asset classes, co-investment opportunities, and terms unavailable to smaller investors, a pattern Fagereng and colleagues document empirically across wealth levels. Meanwhile, the dynasty’s borrowing cost sits near the risk-free floor, because its large liquid collateral makes default risk negligible for lenders. The dynasty therefore captures a spread between what it earns and what it pays to borrow that is wider than what ordinary investors can access — compressed in its favor from both sides simultaneously. Step-up then ensures that spread compounds without fiscal drag across every generational transfer, converting a structural pre-tax advantage into a permanent post-tax advantage by extinguishing the accumulated appreciation on which every other investor would eventually pay capital gains tax.6

III. Who Gets the Benefit

The Death Benefit is not distributed neutrally across the population of asset holders. It flows overwhelmingly to those who already have the most — and within that group, it flows most clearly to those whose estates fall below the threshold at which the estate tax begins to provide even a partial justification for it.

The basic distributional facts

Close to half of all estate value at death consists of unrealized capital gains — gains that were never taxed during the decedent’s lifetime and, under step-up, will never be taxed at all. According to the Congressional Budget Office, in 2019 the top 20% of decedents’ estates received 56% of the total step-up benefit, with the top 1% alone receiving 18% of the total. Among households receiving an inheritance, those with economic income already over $1 million — before the inheritance — expected to inherit an average of $3 million; those with economic income under $50,000 expected to inherit an average of $62,000.7 The 48-to-1 ratio between those figures is not a description of different levels of need. It is a description of how the Death Benefit distributes: to those who already have the most, compounding advantage upon advantage.

The provision labeled a burden — the estate tax, the so-called death tax — touches almost no one. Taxable estate tax returns represented 0.08% of adult deaths in 2019, down from a peak of roughly 7% in 1976. The provision that awards a benefit — step-up in basis, the Death Benefit — flows to a far larger universe of estates carrying appreciated assets below the exemption threshold. The label that dominates public discourse describes a tax that almost no one pays. The benefit that has no label in public discourse flows to estates at every level of the upper wealth distribution, concentrated most heavily at the top.

Two tiers of benefit

The Death Benefit operates differently at different wealth levels, and the difference matters for understanding who it truly serves.

For the merely wealthy — families with $2 million to $10 million in appreciated assets, solidly above the thresholds at which most Americans live but well below the ultra-wealthy — the Death Benefit is usually a single-generation event. A lifetime of appreciated stock, a home purchased decades ago for a fraction of its current value, a small business built and never sold: these pass to heirs with a stepped-up basis, the appreciation permanently forgiven, the heir free to sell without paying the capital gains tax that their benefactor would have owed. The benefit is real and substantial. But it is usually a one-time gift at their benefactor’s death. The merely wealthy do not generally have portfolios large enough to sustain or create the dynastic engine described in the previous section. They receive the Death Benefit once, per generation.

For the ultra-wealthy — families with portfolios large enough to execute the borrow-spend-die strategy across generations — the Death Benefit is not a single-generation event. It is a perpetual wealth-compounding machine. Each generation borrows against appreciated assets, services the debt from portfolio income, dies with the appreciation intact, and passes a fresh-basis portfolio to the next generation to restart the cycle. The benefit is not merely forgiven once. It is forgiven at every generational transfer, compounding the advantage across time without limit and without any fiscal interruption.

The concentration dynamic and its trajectory

The Saez-Zucman wealth distribution data illuminate why this distinction matters. The share of total wealth held by the top 0.1% has returned to levels last seen in 1929 — nearly 20% of all household wealth in the hands of roughly 160,000 families. Meanwhile, the share held by the “merely rich” — families in the top 10% but below the top 1% — has actually declined slightly over the past four decades, even as their absolute wealth has grown. The ultra-wealthy are pulling away not merely from the middle class but from the merely wealthy as well.8

This divergence will deepen. The tax policy changes of recent decades — steadily raising the estate tax exemption, making step-up permanent, and most recently cementing both under OBBBA — may have been intended primarily to confer immediate tax advantages on wealthy donors and constituents. But their long-term structural consequence may prove far more profound than their authors anticipated. The dynastic engine the Death Benefit enables does not merely preserve existing wealth. It compounds it, generation after generation, immune to the market competition and the institutional checks that prevent accumulation from hardening into permanent dynasty.

Today’s extreme fortunes — unprecedented in scale, the product of a specific era of technological and financial concentration — are beginning their multigenerational transmission through a tax arrangement specifically designed, whether intentionally or not, to make that transmission permanent. Step-up is not the only mechanism producing this outcome — housing appreciation, financial concentration, network monopolies, and educational assortativity all play roles — but it is the one examined here, and it is the one that has successfully hidden behind a name that describes something else entirely.

There was a time when a billionaire was considered a financial curiosity — a figure so remote from ordinary experience as to seem almost fictional. Today billionaires number in the thousands, and the world’s first trillionaire may arrive within this decade. The scale is worth pausing on. A single billionaire controls wealth equivalent to one thousand millionaires. A single trillionaire controls wealth equivalent to one million millionaires. When a trillionaire’s wealth grows by $100 billion — as has happened repeatedly in recent years — that single person’s gain equals the entire accumulated wealth of 100,000 millionaires. No corresponding number of millionaires was created. The wealth did not distribute. It concentrated further.

The income alone from such a portfolio is staggering. At a modest 5% annual yield, a trillion-dollar portfolio generates $50 billion each year — enough, at $1 million annually, to support 50,000 families in comfort without selling a single asset. With borrowing against the appreciated principal, even more could be supported — and still without triggering a taxable event. That income stream, taxed as received, is the trickle. The appreciation that step-up permanently forgives at each generational transfer is the flood.

At each generational transfer, the Death Benefit ensures that the concentrated appreciation at the apex will permanently escape capital gains taxation, while the merely wealthy below the apex receive a one-time forgiveness that does not carry the compounding dynastic advantage available only at the top.

Yet even for the largest estates — those that do owe estate tax on the value above the exemption threshold — step-up applies in full to the entire appreciated portfolio. The estate tax is a partial, one-time charge on value above the threshold. The Death Benefit is a permanent, recurring exclusion of appreciation that operates regardless of estate size. The effective estate tax rate on large estates averages well below the 40% statutory rate, given the valuation discounts, family limited partnerships, and charitable vehicles available at that scale. And at every generational transfer, whatever the estate’s size, the first $13.99 million in appreciated assets passes with a fully stepped-up basis and no capital gains tax. No estate tax is owed on that tranche. No capital gains tax will be owed when the heir sells. The appreciation accumulated during the previous generation on that exempt portion is permanently excluded from taxation — not deferred, not reduced, permanently excluded — at every death, in every generation.

The result, projected forward across generations, is not merely a wealthy elite but a dynastically entrenched one — an economic class whose position is not merely the product of market success but of a legal arrangement that makes that position self-perpetuating. The United States has seen great fortunes before. What it has not seen — what the combination of extreme concentration and this self-perpetuating wealth machine may now be creating — is a class of families whose economic dominance is structurally secured against the forces, including taxation, that have historically interrupted the transmission of dynastic wealth.10

IV. The “Taxed Twice” Objection Fails

The most common objection to reforming step-up in basis is that the money was already taxed. The argument runs: the decedent earned income, paid income tax on it, invested the after-tax proceeds, built wealth over a lifetime — and now the government wants to tax it again at death. Double taxation. The family is being penalized twice for the same dollars.

This objection has genuine emotional force. It also fails on its own terms — not as a matter of policy preference but as a matter of arithmetic.

What was actually taxed

Consider the numbers. A person invests $1 million of after-tax income — income on which they have already paid income tax, as the objection correctly notes. That investment appreciates to $10 million during their lifetime. The estate, well below the $13.99 million exemption threshold, owes no estate tax. It passes to the heir with a stepped-up basis of $10 million. The heir sells and pays zero capital gains tax.

What was taxed? Not the original $1 million investment — the after-tax income the decedent earned and invested — it was indeed taxed once, as income, when it was earned.

What was never taxed? The $9 million in appreciation. Not once. Not ever. It accumulated tax-free throughout the decedent’s lifetime — unrealized, untouched, compounding without fiscal interruption — and was permanently excluded from capital gains taxation at death through step-up. The $9 million is not money that was already taxed. It is income that was never taxed at all, but would have been taxed if realized before the benefactor’s death.

The double-taxation objection could apply, at most, to the original $1 million. It has no application whatsoever to the $9 million in appreciation, which is the entire subject of the Death Benefit. Eliminating step-up and replacing it with deemed disposition — taxing the gain at death as if the decedent had sold — would not double tax the original $1 million. It would tax the $9 million once, for the first time, which is all anyone else’s income is taxed.

The objection’s narrow legitimate application

The double-taxation concern does have a narrow legitimate application. For estates large enough to owe estate tax — those above the $13.99 million exemption per individual — the appreciated value of the estate is subject to estate tax at rates up to 40%, only slightly above the 37% ordinary income rate that high-earning wage earners pay on their last dollar of labor income. The estate tax threshold is a gross fair market value test, not a net gain test. An asset purchased for $1 million and now worth $14 million is valued at $14 million for estate tax purposes, with the $13 million in appreciation fully included regardless of what the decedent originally paid. If death were also treated as a realization event for capital gains, the same appreciation would face both estate tax and capital gains tax. That is a genuine design question about the coordination of two taxes on the same economic gain.

The concern is real but narrow. Those subject to potential double-taxation constitute a vanishingly small population — fewer than one estate in a thousand, 0.08% of adult deaths — and for the remaining 99.92%, no estate tax is paid, no coordination problem arises, and the Death Benefit is a pure exclusion of appreciation from taxation with no offsetting tax of any kind. Moreover, the coordination problem can and has been solved: Canada’s deemed disposition regime credits the decedent’s original cost basis against the deemed capital gain, taxes only the appreciation above that basis, and coordinates with any estate-level taxes — taxing the gain once, not twice, at the higher of the applicable rates. A deemed disposition regime in the United States could do the same, in effect restoring step-up to its original 1921 function as a receipt for taxes paid rather than a freestanding reward for dying. The design question merits a solution; it is not a reason to preserve a $72 billion annual benefit for our nation’s wealthiest heirs.

Most importantly, the double-taxation objection as deployed in public debate is almost never about this narrow and rare coordination problem. It is deployed as a general argument against any taxation of inherited wealth, applied indiscriminately to estates of all sizes, the vast majority of which pay no estate tax and face no coordination problem at all. The objection is invoked for the many to protect the few, obscuring the fact that for most estates the question is not double taxation but no taxation.11

The asymmetry with wage income

The appreciation that generates the Death Benefit was also income — economic gain accruing to the asset holder over time. It was simply not realized as taxable cash income. Under a comprehensive income tax, the form of the income should not determine its taxability: a dollar of wage income and a dollar of appreciation are both increases in the holder’s economic position, and both should be taxed only once. Step-up ensures that one of them is taxed once and the other is never taxed at all. A proper concern for double taxation, applied consistently, would require that no single economic gain be taxed more than once as a capital gain — which is precisely what deemed disposition achieves. Applied selectively, as it is in practice, it serves as a justification for taxing neither.12

V. The Wage Earner Has No Equivalent

The Death Benefit is sometimes described as a provision that affects only the very wealthy — a narrow elite whose tax treatment is remote from the experience of ordinary Americans. The distributional data in Section III confirms that the benefit is heavily concentrated at the top. But the structural argument cuts deeper than distribution. The Death Benefit does not merely give wealthy estates a better outcome than wage earners. It creates a parallel tax universe — one in which the fundamental rules governing how income is taxed operate entirely differently depending on how that income was earned and how it is held.

The one-seventh ratio

The aggregate measure of this disparity is striking. Inherited income — income received through bequest and inheritance — is taxed at less than one-seventh the average effective tax rate on income from work and savings.13 That ratio is not the product of a single provision or a single policy choice. It is the cumulative result of a tax architecture that systematically advantages inherited wealth over earned income at every point: preferential capital gains rates during life, the deferral of tax on unrealized appreciation, and the permanent forgiveness of that appreciation at death through step-up. The Death Benefit is the final and most consequential layer of that architecture — the provision that converts a tax preference into a permanent exemption.

For a family executing the dynastic strategy across generations, the effective rate is not one-seventh. It is zero on the appreciated portion of wealth — the component that typically dominates total return. The one-seventh figure is a system-wide average that includes less sophisticated estates and assets that generate taxable income along the way. The full strategy — holding appreciating assets, borrowing to consume, dying with a stepped-up portfolio, restarting the cycle — produces an effective capital gains rate of zero, in perpetuity, across every generation willing and able to execute it. The one-seventh is the average. Zero is the floor, available to those with sufficient wealth to reach it.

What the wage earner cannot do

The contrast with wage income is not merely quantitative. It is structural. A wage earner has no equivalent mechanism. They cannot defer their income until a more favorable moment. They cannot arrange for a lifetime of earnings to escape taxation by the simple act of not spending them. They cannot borrow against their future labor income at favorable rates, service the interest from the income their labor generates, and arrange for the entire principal to be forgiven at death. Every dollar of labor income is taxed in the year it is received, at ordinary rates, without exception.

The appreciation that generates the Death Benefit is economically equivalent to wage income in one fundamental respect: it represents an increase in the holder’s economic position. A worker who earns $100,000 in wages and an investor whose portfolio appreciates by $100,000 are both $100,000 wealthier at the end of the year. The worker pays income tax on their $100,000. The wealthy investor pays nothing — not this year, not next year, and under step-up, not ever. The tax code treats these two identical increases in economic position as categorically different events: one taxable, one permanently exempt. The only relevant difference between them is that one was earned through labor and the other through the passage of time and the ownership of capital.

VI. Other Objections

The family farm and forced sale objection

No discussion of step-up reform is complete without addressing the family farm — the most emotionally powerful argument against taxing gains at death. The argument runs: a family holds farm land that has appreciated enormously over generations. If death triggers a capital gains tax, the heirs will be forced to sell the farm to pay the bill. The family loses the land. The community loses the farm. Reform destroys what generations built.

This argument has genuine human weight behind it. It deserves a direct answer, in two parts.

The first part is empirical. There appears to be no documented evidence that any family farm in the United States has ever been sold to fund federal estate taxes.14 The forced-sale story is politically powerful precisely because it is vivid and sympathetic — but it describes something that does not appear to happen in practice, because the farms it invokes are typically below the estate tax threshold, qualify for existing installment payment provisions, or are transferred within families through mechanisms that defer or reduce the tax liability regardless of reform. The family farm argument has been the most durable objection to estate and inheritance tax reform for decades. It has not been substantiated by a single documented case.

The second part is structural. The forced-sale concern attaches primarily to the estate tax — a tax on the total value of the estate, payable in cash shortly after death. A deemed disposition regime is different in a critical way: it is a capital gains tax on the appreciation, not a tax on the total value, and it can be structured to avoid any forced sale entirely. Canada’s system — the most directly comparable deemed disposition regime — handles farm transfers through a rollover provision: farm property transferred to a child carries over the decedent’s original cost basis, deferring any capital gains tax until the heir eventually sells. No tax is due at death. No sale is required. The gain is deferred, not forgiven — the heir will eventually pay when they sell — but the farm stays in the family for as long as the family chooses to keep it.15

The existing US tax code already contains an analogous provision: installment payment of estate taxes over fifteen years for qualifying farm and closely held business interests. A deemed disposition regime could extend similar treatment to capital gains triggered at death — payable over time, not immediately, with no forced sale required. The administrative tools exist. The forced-sale concern is a design question, not a fundamental objection to taxing gains at death.

The administrative objection

A related objection concerns administrative complexity. The one serious US attempt to move away from step-up — the carryover basis reform enacted in 1976 — was repealed in 1980 before it took effect, after the Joint Committee on Taxation found that compliance required reconstructing the original purchase price of assets potentially held for decades, often without contemporaneous records. The administrative burden was real and the reform was genuinely unworkable as designed.

But this history argues against carryover basis specifically, not against taxing gains at death generally. The 1976 reform failed because it required heirs to reconstruct a dead person’s historical records — an archaeological exercise that was often impossible and always burdensome. Deemed disposition avoids this problem entirely. Under deemed disposition, the taxable gain is the difference between the fair market value at death — a current appraisal, not a historical reconstruction — and the decedent’s adjusted cost basis, which the decedent maintained on their own tax records throughout their lifetime as a living taxpayer. The administrative burden falls on the living taxpayer maintaining their own records — the normal expectation of any taxpayer — rather than on heirs reconstructing records that may not exist. For financial assets, the problem is further diminished by the mandatory cost-basis reporting rules that have applied to brokerages since 2011: the living taxpayer’s basis is already tracked electronically in the brokerage system. The primary remaining appraisal challenge is real estate and closely held business interests — significant, but a far narrower problem than the wholesale basis reconstruction that defeated the 1976 reform.

Canada introduced deemed disposition in 1972 and has operated it for over fifty years without the administrative collapse US opponents predict. The 1976 failure is the history of a specific, poorly designed reform. It is not the history of the approach the essay is describing.16

VII. Tax Neutrality, Not a New Tax

The often-heard suggestion that step-up reform would impose a new tax on inheritance frames such reform as an inequitable “death tax” in a slightly different form. The preceding sections have established that this framing is precisely backwards. The current system is not neutral — and death is not a non-event for taxes. It actively advantages dying over selling, holding over deploying, and inheriting over earning. Reform would not impose a new tax. It would remove an existing subsidy.

The minimal policy argument is this: death should be tax-neutral; neither tax-favored nor tax-punished. The wage earner who receives $1 million in labor income pays income tax on $1 million. The investor who realizes $1 million in capital gains pays capital gains tax on $1 million. The investor who dies with $1 million in unrealized gains pays nothing. Tax neutrality requires that the third outcome be treated like the second — taxed once, at the applicable rate, like everyone else’s income.

The lock-in objection

Step-up is sometimes defended on the ground that it corrects for a distortion the capital gains tax itself creates: the lock-in effect. The capital gains tax gives investors an incentive to hold rather than sell appreciated assets, because selling triggers an immediate tax liability while holding defers it indefinitely. This distortion has real economic costs — capital that would be more productively deployed elsewhere stays locked in existing positions to avoid the tax. Step-up, on this argument, corrects for lock-in by ensuring that at least at death the slate is wiped clean, freeing heirs to redeploy inherited assets without the tax friction that would otherwise deter them.

This argument has a surface plausibility that dissolves on inspection. Step-up does not reduce lock-in. It maximizes it — in a specific and perverse way that the lock-in defense never acknowledges.

Under current law, the rational strategy for any investor holding appreciated assets is unambiguous: never sell. Selling during life triggers capital gains tax immediately, reducing the compounding base by the tax paid. Holding until death triggers the Death Benefit, permanently excluding the gain from taxation. The optimal exit is not any sale during life — it is death. Step-up does not merely fail to solve the lock-in problem. It converts lock-in from a reluctant response to a tax friction into an affirmative wealth-maximizing strategy. The investor who holds rather than sells is not being irrational or sticky. They are executing the dominant strategy the tax code offers.

Eliminating step-up removes this incentive entirely. An investor facing deemed disposition at death — the same capital gains tax whether they sell today or hold until death — has no tax reason to prefer death as the realization event. They can make portfolio decisions on the merits: sell when the capital is better deployed elsewhere, hold when it is not. The lock-in step-up produces is not an incidental byproduct of a well-intentioned provision. It is the predictable equilibrium response to a system that makes dying the optimal financial transaction. Removing the Death Benefit removes the distortion.17

The international comparison

The United States is not alone in having step-up in basis — it is in fact the most common approach among OECD countries that also levy estate or inheritance taxes. But the US combination of unlimited step-up and a near-universal estate tax exemption is distinctive, and the OECD has said so directly. In its 2021 report on inheritance taxation and its 2025 working paper on capital gains, the OECD specifically identified step-up as a provision that should be reconsidered where estate tax exemption thresholds are very high — a description that fits the United States more precisely than any other member country.18

In countries that retain step-up alongside a functioning inheritance or estate tax, the provision has a coherent rationale: the appreciation was taxed at the estate level, and step-up prevents it from being taxed again at the capital gains level when the heir sells. The step-up is a receipt for taxes paid, not a freestanding benefit. In the United States, where the estate tax exemption has been raised to the point that fewer than one estate in a thousand pays any estate tax, step-up has been severed from the tax it was designed to complement. It is no longer a receipt. It is a gift.

Other countries have taken a different path. Canada, when it introduced capital gains taxation in 1972, deliberately chose deemed disposition over step-up — treating death as a constructive sale at fair market value, taxing the gain once, and giving the heir a fresh basis equal to the value on which tax was paid. The Carter Commission, whose report formed the basis for the Canadian reform, expressed the governing principle in a phrase widely attributed to its chair, Kenneth Carter, that has become foundational in Canadian tax policy: “a buck is a buck is a buck.” Income is income regardless of its form, and the tax system should treat it accordingly. Death is a realization event, not an occasion for permanent forgiveness.19

Australia, when it introduced capital gains taxation in 1985, chose carryover basis rather than step-up — deferring the tax until the heir sells rather than forgiving it at death. Denmark and Hungary treat death as a full realization event, consistent with a comprehensive capital gains tax system. New Zealand’s Tax Working Group, when it considered introducing a capital gains tax in 2019, specifically examined and rejected the US step-up model as inconsistent with the principle of taxing economic gains comprehensively.

The international consensus among countries that have thought carefully about this question is that step-up is the wrong answer. Countries that have chosen differently — Canada most prominently — have done so on the principled ground that income should be taxed once regardless of how it is realized, and that the tax system should not make dying the most tax-advantaged financial transaction available.

The revenue picture

The scale of the Death Benefit is not incidental to the policy argument. According to the Congressional Budget Office’s December 2024 budget options report, replacing step-up with carryover basis — deferring the tax until the heir sells rather than collecting it at death — would reduce the deficit by approximately $197 billion over ten years. Replacing step-up with deemed disposition — taxing the accrued gain at death as if the decedent had sold — would reduce the deficit by approximately $536 billion over the same period.20

These are not small numbers. They represent tax that other people — wage earners, savers, investors who sell during their lifetimes, small business owners who realize their gains rather than holding until death — already pay on equivalent economic gains. The Death Benefit does not merely forgive the appreciation in wealthy estates. It shifts the tax burden onto those who cannot or do not execute the holding strategy: those without sufficient wealth to sustain the cycle, those who need to sell to fund retirement or education or a business, those who simply did not have the good fortune to die at the right moment. Every dollar of appreciation permanently excluded at death is a dollar that the existing capital gains rate must recover from a narrower base of realizations. The Death Benefit is not simply a subsidy to wealthy estates — it is a subsidy paid in part by every investor who sells during their lifetime.21

Both reforms represent a fundamental improvement over the current system, and both are worth supporting. Deemed disposition is the more equitable approach: it taxes each generation’s accumulated appreciation at each generational transfer, ensuring the obligation is collected while the gain is still economically present. Carryover basis is less immediately equitable — it permits further deferral — but it ends the permanent forgiveness that is the Death Benefit’s defining feature. The tax obligation follows the asset rather than being extinguished at death.

That distinction matters, however, because dynasties will exploit carryover basis as effectively as they exploit step-up. A family executing the borrow-spend-die strategy never sells. Under carryover basis, the basis carries forward from decedent to heir, then to grandheir, then to great-grandheir — across as many generations as the family continues to hold. The embedded tax liability grows on paper but is never triggered. And crucially, even if some distant generation eventually sells, the time value of money has steadily eroded the real value of what is collected. A capital gains tax on appreciation that accrued decades ago, collected three generations later, may be worth only a small fraction of its face value in present terms. The obligation survives; its economic substance diminishes with each passing generation.

Carryover basis is therefore not a consolation prize but a serious reform — one that would end the dynasty strategy’s most essential advantage for ordinary estates and create at least the prospect of eventual collection even for the largest. If the administrative and political challenges of deemed disposition prove prohibitive, a well-designed carryover basis regime, combined with targeted relief for small estates and illiquid assets, would represent genuine progress. An objection to deemed disposition that converts a critic into a strong supporter of carryover basis is a good outcome for the reform project. The enemy of equity here is not carryover — it is the permanent forgiveness the current system provides.

The pro-capitalist case for reform

This is the point at which the standard framing of step-up reform — as a tax increase on the wealthy, a burden on bereaved families, an attack on the right to pass wealth to one’s children — is most completely inverted.

A tax code that systematically taxes the act of accumulation more heavily than the act of inheritance is not neutral with respect to capitalism’s promise. It is anti-capitalist in a specific and precise sense: it advantages hereditary wealth over productive accumulation, dynastic transmission over the creation of new value, the accident of birth over the exercise of talent and effort. Capitalism’s distinguishing commitment — the universal right to accumulate, open to anyone regardless of birth — is undermined by a provision that makes the return on inherited capital higher, after tax, than the return on newly created wealth. The Death Benefit does not merely distribute unfairly. It tilts the playing field against the very behavior capitalism is supposed to reward.

Reforming it — replacing the Death Benefit with a system that taxes appreciation once, at death or at subsequent realization, like everyone else’s income — is not an attack on capitalism. It is a defense of capitalism. It removes a subsidy to hereditary transmission that the system’s own logic cannot justify. It restores the principle that income is income regardless of its form. And it eliminates the incentive structure through which today’s extreme fortunes are converting themselves into a dynastically entrenched economic class — a class whose position is secured not by continued productive contribution but by the compounding of an inherited advantage that the tax code makes permanent.22

VIII. The Label Inversion

The essays in this series share a structure. Each identifies a fiscal fiction or framing — a legal or accounting artifact that presents a governance choice as an economic necessity, a policy decision as a natural feature of the landscape. The Social Security Trust Fund is not a savings account; it is a political commitment dressed in the language of pre-funding. The debt ceiling is not a fiscal constraint; it is a political tool that was repurposed into a weapon. The government’s ability to create money is not what the standard story describes; the constraints are legal and political choices, not laws of nature.

The Death Benefit follows the same pattern, with one additional feature: it is protected not merely by a fiction about what it is but by a label that names something else entirely. The Trust Fund fiction tells a false story about a real provision. The death tax label tells a true story about a provision that does not exist — and in doing so, makes the provision that does exist invisible.

The death tax does not exist for 999 estates in a thousand. The Death Benefit exists for all of them. But only one has a name in ordinary political discourse, and therefore only one can be retrieved, argued about, defended, or reformed in ordinary political conversation. The label does not merely misdescribe the provision — it occupies the cognitive space where the correct description should be, making it nearly impossible to have the right conversation because the right conversation has no linguistic handle. We are left able to talk only about the thing that is named but does not exist, while the thing that exists and costs the Treasury $72 billion annually remains, for most citizens, simply invisible.23

Naming the benefit is the first act of reform. Not the legislation, not the revenue estimate, not the international comparison — the name. The Death Benefit. A benefit, awarded at death, to those fortunate enough to have been able to spend a lifetime accumulating what they did not need to sell. A benefit with no counterpart in the tax treatment of wage income, no justification in the original logic of the provision that created it, and no defense in the principles of a tax system that claims to treat income equally regardless of its form. A benefit that has survived every serious reform effort for a century because its defenders have successfully prevented the merits from being examined — by ensuring that the benefit has no name in ordinary political discourse.

What the system actually does

Step back from the details — the basis calculations, the deemed disposition mechanics, the estate tax coordination questions — and consider what the current system actually does, stated plainly.

It taxes the wages of a nurse at ordinary income rates, in the year they are earned, without deferral or forgiveness.

It taxes the capital gains of a small investor who sells appreciated stock to fund their retirement, in the year of the sale, at preferential but real rates.

It permanently exempts the lifetime appreciation of a large investment portfolio, accumulated tax-free across decades of compounding, from any capital gains tax — provided only that the holder dies before selling.

It then enables the heirs of that portfolio to borrow against their fresh-basis inheritance at rates unavailable to ordinary borrowers, service the borrowing from portfolio income, and repeat the entire cycle — generation after generation, without any capital gains tax at any generational transfer, in perpetuity.

This is not a neutral system. It is a system that taxes labor and penalizes realization while subsidizing accumulation and rewarding dynasty. It does not merely fail to prevent the emergence of a permanently entrenched economic elite. It is one of the primary mechanisms through which that elite perpetuates itself — through which the fortunes being assembled in this era of extreme concentration will be transmitted, compounded, and dynastically secured across generations that have not yet been born.

A tax system that calls the elimination of this subsidy a “death tax” while calling the subsidy itself nothing at all has successfully named its own loophole out of existence. The fiction here is not about money creation or government borrowing. It is about whose income gets taxed and whose does not — and about a political vocabulary so thoroughly captured by those who benefit from the answer that the question itself has become difficult to ask.

The anti-capitalist core

Capitalism’s distinguishing promise is the universal right to accumulate — the proposition that anyone, regardless of birth, has the right to build wealth through productive activity, and that the system’s institutions will keep that promise open rather than reserving it to those elites who were born into advantage. That promise is what distinguishes capitalism from the aristocratic systems it replaced, in which accumulation rights were the hereditary property of dynastic elites whose position was secured by birth rather than earned by contribution.

The Death Benefit violates this principle not as a side effect but as its central operation. Generation after generation, it ensures that the largest fortunes compound faster than the economy grows, that they pass between generations without capital gains taxation, and that the heirs who receive them begin each cycle with advantages — in borrowing cost, in asset access, in scale — that no newly accumulating investor can replicate. The playing field does not merely tilt. It tilts further at each generational transfer, locked in that direction by a tax provision that rewards the fact of inheritance over the act of creation.

Reforming the Death Benefit is not an attack on capitalism. It is a defense of capitalism — the restoration of a principle that the current system has spent a century quietly abandoning. The principle is simple. It is the principle widely attributed to Canada’s Carter Commission fifty years ago and that every comprehensive income tax system claims to uphold. “A buck is a buck is a buck.” Income is income regardless of its form. And a tax system that exempts one category of income — the appreciation of wealth held until death — from the principle it applies to every other category has not achieved neutrality. It has achieved the opposite: a permanent, compounding, dynastically self-sustaining exception to the rule that everyone pays once, on what they earn, like everyone else.

The death tax does not exist. The Death Benefit does. It is time to call it what it is.24

“By taxing estates heavily at death the State marks its condemnation of the selfish millionaire’s unworthy life.”

— Andrew Carnegie, “The Gospel of Wealth,” North American Review, June 1889. Text via Carnegie Corporation of New York: https://www.carnegie.org/about/our-history/gospelofwealth/

Notes

Joint Committee on Taxation, Estimates of Federal Tax Expenditures for Fiscal Years 2025–2029, JCX-45-25 (2025). The JCT lists the provision as “Exclusion of capital gains at death” and estimates its revenue cost at $66.3 billion in FY2025, $72.5 billion in FY2026, $76.4 billion in FY2027, $79.9 billion in FY2028, and $84.2 billion in FY2029 — a five-year total of $379.3 billion. The provision applies entirely to individuals; the corporate column shows no revenue cost. The essay uses “roughly $72 billion annually” as a shorthand reflecting the FY2026 estimate, but the figure is growing: from $66 billion to $84 billion over the five-year window. The JCT estimate is a static revenue cost — it does not account for behavioral responses, meaning the actual revenue gain from eliminating step-up would differ as investors adjusted their realization behavior. The JCT’s terminology (“Exclusion of capital gains at death”) is more precise than the colloquial “step-up in basis” and directly describes what the provision does: it excludes from taxation the capital gains that accrued during a decedent’s lifetime.↩︎

The cognitive mechanism here is what George Lakoff describes as framing: mental structures activated by language that shape how we perceive and discuss political reality. A concept without a name cannot be activated as a frame and therefore cannot function as an object of political thought or debate. The “death tax” label is a near-perfect instance of what Lakoff calls framing the issue before the debate begins — by the time anyone argues about step-up reform, the frame is already set: taxation at death, burden on families, government taking. The Death Benefit cannot be argued against, reformed, or even defended within that frame because the frame contains no space for it. The provision that exists and does the damage has no linguistic handle in ordinary discourse; the provision that does not exist has one of the most politically effective labels in modern tax policy history. See George Lakoff, Don’t Think of an Elephant: Know Your Values and Frame the Debate (Chelsea Green, 2004).↩︎

The timing precision here is not hypothetical. Under IRC §1014, basis is set at the asset’s fair market value on the date of death. An asset sold the day before death triggers capital gains tax on the full appreciation. The same asset, unsold at death, receives a full step-up. The difference between these outcomes — potentially millions of dollars — is determined by the order of events within a single day. The provision does not merely advantage those who plan to hold until death. It creates a tax cliff at the precise moment of death that can turn an identical economic position into a dramatically different tax outcome depending on timing alone.↩︎

For estates above the exemption threshold — those paying estate tax on the value above $13.99 million per individual — step-up retains a partial coherence as the historical complement to estate tax paid. But even for those estates, the exemption amount itself receives the Death Benefit unconditionally: every estate, regardless of size, receives step-up as a pure benefit on its first $13.99 million in appreciated assets. The portion above the threshold is taxed, imperfectly — the effective estate tax rate averages less than 17%, well below the capital gains rate the decedent would have paid on realized gains during life. Step-up on the taxed portion is at least the historical complement to some tax paid. Step-up on the exempt portion — which covers the entirety of 999 estates in a thousand, and the first $13.99 million of every estate without exception — is the Death Benefit, unqualified and unconditional. The provision designed as a receipt for taxes paid now functions, in the overwhelming majority of its applications, as a substitution for taxation rather than a complement to it.↩︎

The scale advantage compounds this dynamic further. A dynasty borrowing against a $500 million diversified portfolio faces default risk so negligible that lenders charge rates near the risk-free floor — substantially below the rates available to smaller borrowers pledging less diversified collateral at higher loan-to-value ratios. The net spread between portfolio appreciation and borrowing cost is therefore wider for larger wealth holders than for smaller ones, not because their assets are better but because their scale reduces their cost of capital. The strategy is not merely self-sustaining — it is self-amplifying. Each generation inherits a larger portfolio at a fresh basis, can borrow at a lower rate relative to appreciation, and compounds the advantage further. The Death Benefit is the mechanism that converts this pre-tax advantage into a permanent post-tax advantage by ensuring that the surplus the spread generates is never subject to capital gains tax at any generational transfer. Switzerland’s mortgage system illustrates what happens when a structurally similar incentive — maintaining debt against appreciating assets rather than repaying it — is embedded in a tax architecture accessible to ordinary households: the behavior follows at scale, not as sophisticated tax planning but as the rational response to the incentives the tax code creates. The American dynasty strategy requires a wealth level most households cannot reach; the Swiss system demonstrates that the behavior itself, given the right incentives, is entirely ordinary.↩︎

Piketty’s r > g thesis has generated substantial critical literature. The debate centers on three questions: whether r has in fact persistently exceeded g historically (Rognlie argues the apparent rise in capital’s share reflects housing returns rather than broad productive capital); whether r > g is a theoretical necessity or a contingent historical pattern that may not continue; and whether r > g is sufficient to produce increasing concentration absent other institutional factors (Acemoglu and Robinson argue institutions matter more than the r-g spread). What is not seriously disputed is that capital has historically earned returns exceeding economic growth rates in many periods and places, creating a tendency toward concentration absent countervailing forces. The essay uses Piketty’s framework as background context for that tendency — not as a prediction of inevitability. The household-level dynasty argument does not depend on these macro disputes in any case: the borrow-spend-die strategy works whenever a specific large portfolio earns returns exceeding its borrowing cost, which is demonstrably true for large diversified portfolios over long periods regardless of the aggregate r-g relationship. The step-up amplification point is purely mathematical, following from the structure of IRC §1014 and the arithmetic of compound returns. On heterogeneous returns by wealth level, see Fagereng, Guiso, Malacrino, and Pistaferri, “Heterogeneity and Persistence in Returns to Wealth,” Econometrica 88(1) (2020). On the Piketty-to-dynasty connection in the legal literature, see Kades, Eric A., “Of Piketty and Perpetuities: Dynastic Wealth in the Twenty-First Century (and Beyond),” 60 Boston College Law Review 145 (2019). On the borrow-spend-die strategy and step-up, see Yale Budget Lab, “Buy-Borrow-Die: Options for Reforming Tax Treatment of Borrowing Against Appreciated Assets” (2024). The three-layer synthesis presented here does not appear in any of these sources in combined form. For empirical confirmation of the scale of unrealized appreciation in estates, see Gordon, Robert, David Joulfaian, and James Poterba, “Revenue and Incentive Effects of Basis Step-Up at Death: Lessons from the 2010 ‘Voluntary’ Estate Tax Regime,” American Economic Review 106(5) (2016): 662–67.↩︎

Batchelder, Lily L., “Leveling the Playing Field between Inherited Income and Income from Work through an Inheritance Tax,” NYU Law and Economics Research Paper No. 20-11 (2020). The income figures are pre-inheritance economic income, meaning the data describes households that are already high-income receiving the largest inheritances — the Death Benefit flowing toward existing advantage rather than toward need. The 48-to-1 ratio reflects not merely differences in asset accumulation but differences in asset type: high-income households disproportionately hold appreciated financial assets and business interests — precisely the assets for which step-up provides the greatest benefit — while lower-income households hold assets whose value lies primarily in their use rather than in accumulated unrealized appreciation.↩︎

Saez, Emmanuel, and Gabriel Zucman, “Wealth Inequality in the United States since 1913: Evidence from Capitalized Income Tax Data,” Quarterly Journal of Economics 131(2) (2016). The finding that the merely rich have lost relative ground to the ultra-wealthy — with fortunes of $20 million or more growing much faster than those of only a few million — is consistent with the scale-advantage mechanism described in footnote 5: larger portfolios sustain lower-cost borrowing, earn persistently higher after-tax returns, and benefit most powerfully from a step-up provision that ensures their appreciation is never subject to capital gains tax at any generational transfer. The Death Benefit does not merely reflect existing wealth concentration; it contributes to its acceleration.↩︎

[deleted]

The distributional asymmetry extends to the loss side of the ledger as well. Under current law, an heir who inherits a highly appreciated asset receives it at its stepped-up date-of-death value as their cost basis. If the asset subsequently declines in value, the heir may claim a capital loss — a deduction against taxable income — measured from that stepped-up basis. The decedent’s lifetime gain was forgiven at death. The heir’s post-death decline is deductible. The Treasury collected nothing on the appreciation and subsidizes the subsequent decline. The asymmetry runs in the same direction at every point: gains accumulated during life escape at death; losses incurred after death are deductible. This is not an incidental feature. It is the logical consequence of a system structured so that the estate is never on the wrong side of a tax transaction. Heads the dynasty wins; tails the Treasury loses.↩︎

The rhetorical deployment of the double-taxation objection follows the pattern identified throughout this series: a concern that has genuine application in a narrow, specific case is generalized into a universal principle that protects a far broader population than the concern actually covers. The Trust Fund argument — Social Security is pre-funded — applies at most to current retirees who paid into the system at specific contribution rates; it is deployed to foreclose any discussion of fiscal policy. The double-taxation argument applies at most to the tiny fraction of estates above the exemption threshold; it is deployed to foreclose any discussion of step-up reform. In both cases, the specific concern provides cover for a general position whose beneficiaries extend far beyond those for whom the concern is legitimate.↩︎

The Haig-Simons definition of income — the standard academic formulation underlying most comprehensive income tax theory — defines income as consumption plus change in net worth over a period. Under this definition, unrealized appreciation is income as it accrues, regardless of whether it is realized as cash. The US income tax departs from the Haig-Simons ideal by taxing only realized gains, a concession to administrative practicality and the liquidity constraints that would arise from taxing paper gains annually. Step-up converts this administrative concession — deferral of tax until realization — into a permanent exemption by making death a non-realization event. The concession to practicality becomes a gift to dynasty. Deemed disposition restores the realization requirement without requiring annual mark-to-market taxation: the gain is deferred during life, as under current law, but taxed once at death rather than permanently forgiven.↩︎

Batchelder (2020), cited in footnote 7. The one-seventh figure reflects the combined effect of preferential capital gains rates, the deferral of tax on unrealized appreciation during life, and the permanent forgiveness of that appreciation at death through step-up. It is a system-wide average across all inherited income; for estates executing the full dynastic strategy described in Section II, the effective rate on appreciated capital is zero.↩︎

Thomas, Kathleen DeLaney, “Tax and the Myth of the Family Farm,” 110 Iowa Law Review 1811 (2025), published May 15, 2025, https://ilr.law.uiowa.edu/volume-110-issue-4-1/2025/05/tax-and-myth-family-farm. Thomas conducts a comprehensive review of available evidence and finds no documented case of a family farm sold to fund federal estate taxes — language drawn directly from the paper’s abstract. The finding is consistent with the structure of the estate tax: the $13.99 million per-individual exemption excludes virtually all working family farms from estate tax liability, and those few farms above the threshold qualify for installment payment provisions under IRC §6166 that allow estate taxes to be paid over fifteen years. The forced-sale narrative has persisted for decades in political debate without empirical foundation.↩︎

Under the Canadian Income Tax Act, farm or fishing property transferred to a child may be elected at any amount between the property’s adjusted cost base and its fair market value, allowing the capital gain to be reduced to zero at the executor’s discretion. The child takes over the parent’s cost basis and pays capital gains tax only when they eventually dispose of the property. A lifetime capital gains exemption of $1.25 million (indexed to inflation as of 2024) further reduces or eliminates the tax on qualifying farm property when it is eventually sold. The combination — rollover deferral plus a substantial exemption — means a genuine working family farm transferring to the next generation faces either no immediate tax or a substantially reduced one, while the provision that produces the American Death Benefit — permanent forgiveness of unlimited appreciation for large investment portfolios — does not exist in the Canadian system.↩︎

The 1976 Tax Reform Act replaced step-up with carryover basis effective for deaths after December 31, 1976. Implementation was immediately delayed, then repealed retroactively by the Crude Oil Windfall Profit Tax Act of 1980 before it had taken effect for a single estate. The Joint Committee on Taxation’s analysis identified two primary problems: the difficulty of establishing the decedent’s original basis for assets held for many years without adequate records, and the administrative burden on executors required to gather that historical information across potentially large and diverse estates. Neither problem applies to deemed disposition, which requires only a current appraisal of fair market value at death — a standard element of estate administration regardless of the tax treatment of gains — and the decedent’s adjusted cost basis as maintained on their own tax records during life. The basis-reconstruction problem is further diminished for financial assets by the mandatory cost-basis reporting rules that have applied to brokerages since 2011 under Section 403 of the Energy Improvement and Extension Act of 2008, Division B of Public Law 110-343, 110th Congress (enacted October 3, 2008), which added IRC §§ 6045(g), 6045A, and 6045B requiring brokers to report customers’ adjusted basis in securities transactions: covered securities purchased after the relevant effective dates have electronically tracked bases already in the brokerage system. The primary remaining challenge is real estate and closely held business interests, both of which require appraisal regardless of the tax regime. The United States has one brief empirical data point on carryover basis in practice: the 2010 estate tax lapse. Under the Economic Growth and Tax Relief Reconciliation Act of 2001, the estate tax was eliminated entirely for deaths occurring in calendar year 2010, with a modified carryover basis regime substituted — heirs received the decedent’s original basis rather than a stepped-up basis, subject to a $1.3 million general basis increase allowance and an additional $3 million for assets passing to a surviving spouse. Gordon, Joulfaian, and Poterba’s analysis of estates that filed under the 2010 regime found that unrealized capital gains accounted for roughly 44% of the fair market value of non-cash assets, with many of the largest gains on assets held for at least two decades — empirically confirming the scale of appreciation that step-up forgives in typical large estates. The 2010 experience also documented that carryover basis was administratively manageable for financial assets, where brokerage records preserved original purchase prices, while creating genuine difficulties for real estate, closely held businesses, and assets acquired through prior inheritances — consistent with the essay’s argument that the administrative challenge is concentrated in illiquid assets rather than the broad asset universe. The 2010 lapse was an imperfect experiment: widely anticipated years in advance, giving wealthy families time to plan around it, and lasting only one year. But it is the only real-world test of carryover basis on actual US estates, and its results support rather than undermine the case for deemed disposition. Two further design questions deserve acknowledgment. First, if asset values fall between the date of death and the date of distribution to heirs — a genuine risk for illiquid assets where probate can take months or years — heirs could face a tax bill calculated on a value that no longer exists. A valuation election allowing heirs to use the lower of date-of-death value or distribution-date value, or installment payment provisions analogous to IRC §6166, would address this without requiring the gain to be forgiven entirely. Canada’s spousal rollover and farm property rollover elections provide working models. Second, for heirs whose primary inherited asset is a modestly appreciated home or small investment account, a deemed capital gains tax could consume a meaningful fraction of a modest inheritance. A specific exemption for the first tranche of inherited appreciation per recipient — analogous to Canada’s $1.25 million lifetime capital gains exemption for qualifying farm and small business property — would protect ordinary heirs while preserving the deemed disposition tax for the large appreciated positions that are the primary policy target. Both problems are genuine and soluble; neither constitutes a fundamental objection to deemed disposition, only a calibration challenge that other countries have addressed successfully.↩︎

The lock-in effect of the capital gains tax is a genuine and well-documented distortion. The correct remedy, however, is not a permanent exemption concentrated at death and at the top of the wealth distribution, but a more neutral realization regime — one that does not privilege any particular moment of realization over others. If capital gains rates are thought to be too high for moderate-income investors, the appropriate remedy is a progressive rate structure that reduces the rate for smaller gains while maintaining it for the large unrealized positions that account for most of the step-up benefit. Capital gains preferences are defensible as an incentive for ordinary household investment and risk-taking; they are not defensible as a permanent subsidy for dynastic wealth accumulation. The current system does not achieve a sensible balance between these objectives. It eliminates the tax entirely for the largest and most concentrated gains — those held until death — while taxing smaller realizations during life at rates that create genuine lock-in for ordinary investors. A reform that replaced step-up with deemed disposition and used the resulting revenue to lower capital gains rates on lifetime realizations would reduce lock-in at the bottom of the distribution while eliminating the dynastic exemption at the top.↩︎

OECD, Inheritance Taxation in OECD Countries, OECD Tax Policy Studies No. 28 (2021), https://doi.org/10.1787/e2879a7d-en; Hourani, Diana, and Sarah Perret, “Taxing Capital Gains: Country Experiences and Challenges,” OECD Taxation Working Papers, No. 72, OECD Publishing, Paris, February 25, 2025, https://doi.org/10.1787/9e33bd2b-en. The 2021 inheritance report states in Section 4.2.9 (“Tax treatment of unrealised capital gains at death”) that “the step-up in basis should be reconsidered, particularly where inheritance or estate taxes are not levied, or where inheritance or estate tax exemption thresholds are very high” — language that describes the post-OBBBA United States with precision. Note that the OECD uses “should,” a stronger recommendation than the “could” sometimes cited in secondary sources. The 2025 Hourani paper further identifies step-up as a provision that “significantly adds to lock-in effects in countries where it applies” (Section 4.2, p. 25) — directly contradicting the standard US defense that step-up reduces lock-in.↩︎

Royal Commission on Taxation (Carter Commission), Report of the Royal Commission on Taxation, 6 vols. (Ottawa: Privy Council Office, 1966). The Commission was chaired by Kenneth LeM. Carter, a Toronto tax lawyer and accountant. The phrase “a buck is a buck is a buck” is attributed to Carter in Canadian official discourse — including Canada’s 2024 federal budget and the Deputy Prime Minister’s remarks on capital gains reform — and is treated as the foundational expression of the Commission’s comprehensive income tax framework. The Canadian Tax Foundation describes it as a summary of the Commission’s views rather than a verbatim quotation; the specific location within the six-volume report has not been pinpointed in secondary literature, which cites Macdonald, Les, “Royal Commission on Taxation,” Canadian Encyclopedia, February 7, 2006, as the source for the attribution. The phrase is a riff on Gertrude Stein’s “a rose is a rose is a rose.” Whether Carter’s own words or an apt summary of his position, the principle is unambiguous: a dollar of wage income and a dollar of capital appreciation are both increases in economic capacity and should be treated identically for tax purposes. The deemed disposition rule at death is the direct application of this principle to the realization question: if gain is income, and income should be taxed once, then the permanent exclusion of gain from taxation at death is a departure from the principle the tax system should not permit.↩︎

Congressional Budget Office, “Change the Taxation of Assets Transferred at Death,” in Options for Reducing the Deficit: 2025 to 2034 (December 12, 2024), https://www.cbo.gov/budget-options/60943. The CBO presents two alternatives: carryover basis (heirs inherit the decedent’s adjusted basis and pay capital gains tax when they sell), estimated to reduce the deficit by $196.9 billion over 2025–2034; and deemed disposition (gains taxed as if the decedent had sold at death, included in the decedent’s final income tax return, with a deduction from estate taxes to avoid double taxation), estimated to reduce the deficit by $536.1 billion over the same period. Note that the underlying revenue estimates were produced by staff of the Joint Committee on Taxation. Both figures are static estimates that do not account for behavioral responses — the additional realizations that would occur during life once the incentive to hold until death is removed. The carryover basis alternative phases in slowly because it only affects assets acquired after the effective date; the deemed disposition alternative raises substantially more revenue by taxing the full stock of accumulated unrealized gains at each death.↩︎