The Government Can’t Print Money — Or Can It?

How a Legal Choice Became a Law of Nature, and Who Benefits from the Confusion

The government you live under does not work the way you were taught. This series examines the gap — not to assign blame, but to make democratic deliberation possible. You cannot evaluate options you do not know exist.

The first essay, “The Trust Fund Is a Comfortable Lie — and We’re Paying for It in Confused Citizens,” showed how the Social Security Trust Fund encodes a gold-standard fiction into a fiat-currency world — making a political commitment look like a savings account, and making “the money is already there” a reassurance that conceals a choice. The second essay, “The Debt Ceiling Was Built to Help Treasury Borrow — Then Someone Found the Gun,” showed how a tool of congressional humility became a weapon of extortion — and how the constraint it appears to impose has no economic content, only political utility.

This essay continues the series. The first two examined fictions about what the government must do — that it must pre-fund Social Security, that it must borrow before it can spend. This essay examines a fiction about what the government cannot do: create money. The prohibition turns out to be a legal choice rather than an economic law. The practice turns out to be already occurring, at multi-trillion dollar scale, under a different name. And the choice of covertness over transparency turns out to serve specific interests that have nothing to do with the inflation risk invoked to justify it.

More essays will follow. The fiscal fictions examined here — about savings, about borrowing, about money creation — are the foundation on which a larger set of convenient fictions about taxation has been built. Those arguments are easier to make once this foundation is visible.

The Received Wisdom

Everyone knows the government can’t print money. Printing money causes inflation. The Weimar Republic printed money and destroyed its currency. Zimbabwe printed money and produced billion-dollar loaves of bread. The United States government, by contrast, is constrained to obtain funds the responsible way: through taxation, which raises money from citizens, or through borrowing, which raises money from investors who expect to be repaid with interest. These are the two options. They are the whole menu.

Politicians across the spectrum repeat this as settled fact. Budget debates proceed entirely within it. When a spending proposal is challenged as unaffordable, “we can’t print money” is offered as the terminal argument — the appeal to a law of nature that ends the discussion. It is the fiscal equivalent of gravity: not a policy choice, not a legislative artifact, but a feature of economic reality that no government can repeal.

This essay is about that claim. Not about whether printing money is wise — it often isn’t. Not about whether inflation is a real constraint — it is, and an important one. Whether “the government cannot create money” describes an economic law or a legal choice is the question. Whether the prohibition is what it appears to be.

The Trust Fund essay showed that the government’s fiscal commitments are political rather than actuarial. The debt ceiling essay showed that the constraint on borrowing is nominal rather than real — that a ceiling unadjusted for inflation or economic growth has no coherent relationship to real fiscal capacity. This essay shows that the constraint on money creation is legal rather than economic. It also shows something else: the prohibition on printing money does not prevent the government from printing money. It requires the government to pay Wall Street for the privilege.

The argument has three layers: what the law actually says, what the government actually does, and what a better system would look like. None of these is the story most citizens have been told.

What the Law Actually Says

Before reaching the statutes, the basic operational constraint deserves a clear statement, because it is not a law at all. Treasury, like any bank customer, can only spend from balances in its bank account — the Treasury General Account (TGA) at the Federal Reserve — and can only increase its balances through the same mechanisms available to any bank depositor: receiving payments such as tax receipts, or receiving the proceeds of borrowing. Banks do not provide their customers, public or private, with the ability to create money in their own accounts. Only banks, and the Federal Reserve, can create money because only banks can issue the deposit liabilities that function as the primary medium of exchange in our economy. This is not a statutory requirement. It is a consequence of how the modern payments system works.

It was not always so. During the Civil War, the Legal Tender Act of 1862 authorized the Treasury to print $450 million in paper fiat currency — United States Notes, known as Greenbacks — and declare them legal tender. The government could act as its own bank because it was printing physical currency and handing it directly to soldiers, suppliers, and contractors. That avenue closed during the late twentieth century, with the final issuance of United States Notes wrapping up in 1971 and Congress permanently repealing the Treasury’s note-reissuance requirements in 1994 (Pub. L. 103–325, title VI, §602(f)(4)(B)). In the modern digital economy, nearly all money exists as electronic ledger balances clearing through Federal Reserve Banks. Treasury cannot hand out paper scrip to pay its bills. It must credit digital accounts, and those accounts are controlled entirely by the Federal Reserve and the commercial banking network. The operational constraint on government money creation is therefore real — but it is largely a consequence of the architecture of the modern payments system, not of any specific statute prohibiting money creation.¹

Yet physical currency issuance is not the only way Treasury could create money. If Treasury could sell securities directly to the Fed, the Fed would credit the Treasury General Account in exchange, effectively creating money for government use. The natural instrument for such a transaction is a zero-interest perpetual bond — a consol — that carries no coupon payment and no maturity date. It would cost Treasury nothing to service and would impose no future repayment obligation. A consol issued directly to the Fed in exchange for a TGA credit would be, in economic substance, government money creation: new purchasing power appearing in Treasury’s account, backed by an obligation that generates no cash drain.

For the first two decades of the Federal Reserve System, the authority to purchase debt directly from the Treasury was highly ambiguous even though it was frequently utilized during wartime and tax seasons. While the Emergency Banking Act of 1933 explicitly authorized direct purchases, the arrangement was abruptly halted by the Banking Act of 1935. A Senate committee amendment prohibited direct purchases and required that all Fed purchases of Treasury obligations occur only in the “open market” — through secondary market transactions with private dealers, not from Treasury itself. The committee report stated only that the provision “has been modified so as to provide that direct obligations of the United States may be purchased only in the open market.” One sentence. No reasoning. No floor debate for or against it.

When insiders were later asked why the prohibition was inserted, they gave three different answers. Marriner Eccles suggested it was inserted at the request of government securities dealers, who stood to lose business if Treasury could bypass them and deal directly with the Fed. W. Randolph Burgess thought it was meant to limit Federal Reserve balance sheet expansion. Others believed it was aimed at discouraging deficit financing by forcing Treasury into the market. These explanations, offered as much as twelve years after the fact by people who were present, are irreconcilable. The prohibition’s rationale was never publicly argued, never authoritatively settled, and has remained contested ever since. Nonetheless, Congress recognized the usefulness of direct purchases and temporarily restored a limited direct purchase authority during World War II, capping it at $5 billion and renewing it periodically through the postwar years until the exemption finally lapsed on June 1, 1981. The constraint the public treats as a law of nature is younger than many voters and has been reversed before. But the timing is suggestive. Most Depression-era reforms moved revenue away from Wall Street; this one moved revenue toward it, at the moment when dealer transaction volumes had collapsed and the provision’s beneficiaries needed it most — inserted without public debate into a bill whose controversy was focused entirely elsewhere.²

Whatever the reason for the open-market requirement, it is much more than a mere procedural inconvenience — it imposes a genuine market discipline that direct purchase would not. Treasury must issue debt that private buyers will accept at the offered terms before the Fed can acquire it from the open market. A zero-interest consol issued to raise funds directly from the Fed would fail entirely in the open market: with no coupon and no maturity, it offers the buyer no economic return. One might imagine selling such a consol at a discount — but discounting an instrument with no future cash flows at all means discounting it to zero, which defeats the purpose of issuing it. The open-market requirement therefore means that the natural instrument for transparent monetary financing — the zero-interest consol — is precisely the instrument that private markets will never buy and thus that the Federal Reserve will never have the opportunity to purchase. Treasury must attach interest sufficient to attract private buyers, creating future fiscal obligations and financing costs. The cheapest and simplest monetary financing option is permanently out of reach.

Layered atop this is the debt ceiling, examined in the previous essay: even the permitted route of borrowing is capped by a nominal dollar figure that adjusts for nothing. The ceiling does not prevent money creation directly; it constrains the one financing channel that the other structures have left open.

The governance structures surrounding these mechanics — statutory prohibitions, central bank independence, market discipline, debt limits — are real and consequential. The result is not a coherent system designed to enforce a sound economic principle. It is a stack of historical accidents, unexplained operational constraints, and institutional sediment, each layer serving its own purpose at its own moment, producing in combination a result that has been naturalized into apparent economic law. But together they describe how humans have chosen to regulate the monetary system, not what the monetary system or economics requires. The public narrative conflates these two things, presenting governance constraints as operational impossibilities, as if the law of the land were also a law of physics.

What Actually Happens: The One-Way Mirror

Here is what the law actually prevents: the Federal Reserve purchasing Treasury securities directly from Treasury at the moment of issuance, crediting the Treasury General Account with newly created reserves.

Here is what the law does not prevent: the Federal Reserve purchasing those same Treasury securities from Goldman Sachs two days after Goldman Sachs purchased them from Treasury.

In both cases, Treasury has issued a bond and received money. In both cases, the Fed holds the bond and has created new reserves. The only difference is that Goldman Sachs held the bond for forty-eight hours and collected a spread for its trouble.

The Federal Reserve’s balance sheet expanded from roughly $900 billion in 2008 to $9 trillion by 2022, an increase of more than $8 trillion, through four rounds of quantitative easing. In each round, the Fed purchased Treasury securities and other assets from financial institutions, crediting those institutions’ reserve accounts with newly created money. Treasury, having sold those bonds to the same institutions days or weeks earlier, had already received the proceeds and spent them. The circuit runs: Treasury issues debt, the public buys it, the Fed buys it from the public, the public has cash instead of bonds, Treasury has spent the money. Those reserves did not come from some pre-existing pool of Fed savings. They were created at the moment of purchase by a bookkeeping entry that expanded both sides of the Fed’s balance sheet simultaneously — assets up by the value of the bond, liabilities up by the value of the newly credited reserves. This is what “printing money” means in a modern payments system: not a physical press, but a keyboard entry that brings new money into existence.

The same mechanism applies when the Fed buys commercial debt — mortgage-backed securities, agency bonds, corporate paper. All of it is purchased with newly created reserves. All of it generates income that the Fed is required by statute to remit to Treasury after covering its expenses, making the federal government the effective beneficiary of private-sector interest streams that the Fed has monetized on its behalf.

This is monetary financing. It is called quantitative easing, open market operations, asset purchase programs — anything but what it is. The IMF’s own 2022 research paper acknowledged exactly why the labeling matters: “central banks do not employ monetary financing in a transparent manner and following theory prescriptions,” which is why “the analysis cannot easily pinpoint historical episodes of monetary financing.” The practice is occurring. It is not being labeled as what it is.³

Paul Sheard, at the time S&P’s chief global economist, put the mechanics plainly in a 2014 paper: QE “involves the central bank creating bank reserves to acquire assets,” and this “does sound at least like the electronic printing of money.” He went on to argue that QE differs from true monetary financing — that argument comes below — but his concession of the mechanics is the starting point.⁴ Adair Turner, former chairman of the UK Financial Services Authority, presenting at the IMF’s own annual research conference in 2015, went further: “the technical feasibility and desirability in some circumstances of monetary finance is not in doubt,” and “all the really important issues are political.”⁵ Among those who have actually conducted the technical debate, the question is no longer whether the government can create money. The question is whether it should do so openly.

The monetary sovereign proxy. Considered as a whole, the Federal Reserve performs operationally everything that a monetary sovereign does. It creates money from nothing, acquires assets with those created reserves, earns income on those assets, and remits that income to Treasury. When its interest expenses exceeded its income during 2022 to 2025 — rates having risen above the yields on its QE-era bond portfolio — it continued paying its obligations by crediting reserve accounts, because it cannot be insolvent in the currency it issues. The “deferred asset” that appeared on its balance sheet during that period was an accounting convention. The Fed was never at risk of being unable to pay. It created the reserves needed and recorded the excess as a balance sheet entry to be recovered from future earnings. This is precisely what a monetary sovereign does.¹¹

The United States government has built a legal architecture that prohibits it from acting openly as a monetary sovereign. Simultaneously it has created an institution — the Federal Reserve — that acts as its monetary sovereign proxy, performing all the same operations under a different label. The cost of conducting monetary sovereignty through a proxy rather than directly is the broker tax: every dollar of effective monetary financing must pass through the primary dealer oligopoly, which collects a spread at auction and another on the resale to the Fed. Billions of dollars annually flow to a licensed group of financial institutions as the price of maintaining the fiction that the government is not doing what it is doing.⁶

The private toll. The primary dealer system creates a structural oligopoly within the Treasury market. A select group of roughly two dozen designated financial institutions — Goldman Sachs, JPMorgan, Citigroup, and their peers — are the only participants required to bid in every Treasury auction, making them the guaranteed backstop for every issuance. More importantly for this essay’s argument, they are the exclusive counterparties for Federal Reserve open market operations: when the Fed buys Treasury securities, it buys only from primary dealers, not from the broader universe of auction participants. Foreign governments, pension funds, and other direct bidders who purchased at auction must sell through primary dealers to reach the Fed. The dealers collect a spread on both legs of that round trip.

During QE periods when the Fed was purchasing $80 to $120 billion of Treasuries each month, the aggregate dealer spread on those transactions represented billions of dollars annually — a private fee on what is, in economic substance, a government financing operation.¹⁴ The open-market requirement does not prevent monetary financing. It requires that monetary financing be conducted through a channel that makes it profitable for a specific, small, licensed group of financial institutions. The prohibition is not a wall between the government and a dangerous practice. It is a one-way mirror. The practice occurs on one side; the public is told it does not exist on the other. And a private toll is collected at the glass.

Is QE Really Monetary Financing? The Permanent/Reversible Question

The most sophisticated objection to QE as monetary financing is that QE is categorically different from true monetary financing because QE is explicitly designed to be reversed. The Fed can sell back its Treasury holdings at any time, extinguishing the reserves it created. True monetary financing — such as helicopter money or direct central bank fiscal transfers — is intended to be permanent. In this view, a central bank that can and will unwind its asset purchases is merely managing liquidity, not financing the state.

Certainly, a central bank that creates reserves with the genuine intention to reverse the operation when conditions normalize is doing something conceptually different from one providing a permanent fiscal transfer. The credibility of that reversal commitment is what separates monetary policy from monetary financing, and the distinction is not cosmetic.

The reality, however, is a complete inversion of these theoretical labels: “permanent” fiscal injections are routinely destroyed through taxation, while “temporary” monetary balances show a stubborn tendency to become permanent.

Consider helicopter money — the textbook definition of a permanent fiscal transfer. The moment those dollars are spent into the economy, they immediately enter the regular stream of national commerce, where they are relentlessly drawn down and extinguished by federal taxation. Helicopter money is only as permanent as the tax code allows it to be. Conversely, Federal Reserve QE balances — explicitly advertised as temporary liquidity injections — have exhibited a stark ratchet effect over the last two decades, with each crisis establishing a higher baseline floor that is never fully dismantled, as the chart below makes visible.

This empirical breakdown reveals that permanence is the wrong criterion for evaluating monetary financing instruments altogether. Helicopter money, zero-interest consols, and QE reserves are all subject to the same macroeconomic withdrawal mechanism: federal taxation, which extinguishes currency regardless of the accounting pipeline that birthed it. The relevant criterion is never “will this instrument exist forever?” but always “what do current economic conditions require?” — the fundamental question Abba Lerner frames in his Functional Finance writing, and one whose answer remains identical across every instrument.⁷ The permanent-versus-reversible distinction is not a boundary line of economic law. It is a minor difference in transmission mechanics. And unlike the reversibility of QE — an informal commitment with no legal mechanism to enforce it against a future Fed that chooses otherwise — an explicit statutory instrument governed by clear conditions is both more honest about what it is and more governable in practice.

What monetary financing actually is. The permanence test — distinguishing QE from helicopter money by whether reversal is intended — imports the commodity-currency mental model through the back door. It treats “real” financing as something that gets fully repaid and monetary financing as something that doesn’t. Under Lerner’s Functional Finance, repayment is secondary to economic conditions. Whether a monetary instrument is retired next year or in fifty years depends on what conditions warrant, not on what label was applied at issuance.

The consolidated balance sheet provides the right criterion. All Fed holdings of Treasury securities constitute monetary financing, because all share the same economic character: the Fed is a government institution that remits its earnings to Treasury, so debt the Fed holds generates interest that flows in a circle. The government owes money to an institution that returns the money. Whether this arrangement will be wound down in five years or fifty or never is a question about future monetary policy, not about current economic substance. The Fed’s $4.3 trillion in Treasury holdings represents $4.3 trillion of government self-financing — the figure that the standard public debt measures systematically obscure.

The Weimar problem. The objection that terminates most public discussions of monetary financing must be met directly: the experience of Weimar and Zimbabwe. Both cases are real. Both involved money creation that produced catastrophic hyperinflation.

The examples are real, but the inference is wrong. What Weimar Germany and Zimbabwe shared was not money creation per se — it was money creation in economies that had already lost the productive capacity to absorb additional demand. Germany in 1923 was paying war reparations in foreign currency while its industrial base was under foreign occupation. Zimbabwe in 2008 had experienced a collapse in agricultural output following land confiscation and the flight of skilled workers. In both cases, money was being created to purchase goods and services the domestic economy could not supply. More money chased fewer goods: the definitional mechanism of inflation.

The United States in 2009, after a year of QE1, with unemployment above 10 percent and the economy operating far below capacity, was not comparable on any economically relevant dimension. The economy had vast unused productive capacity — workers, factories, office space — capable of absorbing additional demand without bidding up prices. The Federal Reserve created roughly $3.5 trillion in reserves through QE1 to QE3. Inflation averaged below 2 percent throughout the period. The AIER cites Venezuela and Zimbabwe as the inevitable destination of any monetary expansion but does not explain why $3.5 trillion in QE produced a decade of below-target inflation rather than hyperinflation. The answer, which Abba Lerner articulated in his 1943 paper “Functional Finance and the Federal Debt,” is that the relevant variable is not the money supply but productive capacity. Create money when the economy has slack to absorb it; do not when it does not. The constraint is real. It just is not the constraint that “printing money causes inflation” implies.⁷

What Transparent Instruments Would Look Like — And How to Govern Them

Given that monetary financing already occurs at multi-trillion dollar scale, the question is not whether to permit a dangerous new practice. The question is whether to conduct an existing practice transparently.

Two instruments have been proposed in the serious literature as vehicles for transparent monetary financing. Both are simpler than what the government currently does.

The first is the platinum coin. 31 U.S.C. §5112(k) authorizes the Secretary of the Treasury to mint platinum coins in accordance with “such specifications, designs, varieties, quantities, denominations, and inscriptions as the Secretary, in the Secretary’s discretion, may prescribe.” No denomination limit is specified. A Treasury secretary could mint a coin with a face value of $1 trillion, deposit it with the Federal Reserve, and the Fed would credit the Treasury General Account accordingly — no bond issued, no interest obligation, no maturity date. Whether this particular authority extends to this particular use is contested. It is also suggested by some that the Federal Reserve would refuse to accept the coin for deposit. The point is that the debate is about legal interpretation, not about economic possibility.

The second and more serious candidate instrument is the zero-interest perpetual consol — a bond with no coupon and no maturity date, issued by Treasury to the Fed in exchange for a credit to the Treasury General Account. Paul Sheard, writing in 2014, described exactly this instrument as the natural implementation vehicle for monetary financing, calling it “nonmarketable zero-coupon perpetuities to the central bank.”⁴ Adair Turner, presenting at the IMF in 2015, described the same thing as “a non-interest-bearing non-redeemable due from government receivable.”⁵ Two senior mainstream economists, writing independently, arrived at the same instrument as the obvious description. Making it a legal instrument of Treasury financing would formalize what the serious literature already treats as standard. The zero-interest consol is also economically superior to the current interest-bearing arrangement for the consolidated government in every rate environment — the objections to it are institutional and political rather than economic.

The coin and the consol are economically identical. Both create purchasing power for the government at zero net cost, require no future interest payments and no principal repayment, and could be retired — the coin melted, the consol cancelled — when economic conditions warrant.

If Treasury issued these instruments when conditions warranted and retired them when conditions required, the outstanding stock at any moment would be a public ledger of accumulated monetary financing decisions. This number currently exists nowhere in honest form. The IMF acknowledged that opacity prevents empirical analysis of monetary financing episodes, because the practice cannot be studied when it is not labeled as what it is.³ An explicit stock, published and tracked, would give citizens something currently absent: a visible, auditable account of how much money the government has created for fiscal purposes.

The most common objection to transparent monetary financing is the credible-commitment problem: to be stimulative, monetary financing must be credibly permanent, but to be safe from inflation, the central bank must retain the ability to reverse it. Critics argue these requirements are irreconcilable.

The framing asks the wrong question. Whether the government can make a credible commitment to permanence is genuinely uncertain. But whether the government can make a credible commitment to rationality — to doing what economic conditions require — is not. Central banks make exactly this kind of commitment routinely, with genuine market credibility. The Fed’s forward guidance ties policy to observable economic indicators. No one argues that interest rate policy faces an insoluble credibility problem because the Fed might someday change rates.

Monetary financing can be governed by the same structure. Given three economic states, there are three responses: when the economy is below capacity and inflation is below target, monetary financing is appropriate and the commitment not to reverse is credible because withdrawal would be contractionary and nobody wants that; when the economy is approaching capacity and inflation is rising, new monetary financing stops and the stock held stable; when the economy is at or above capacity and inflation is at or above target, withdrawal of monetary financing is appropriate and benign — the economy can absorb monetary contraction precisely because it is running hot, so there is no paradox in the commitment to reverse under those conditions. The commitment would not be “this money will never be withdrawn,” it would be “this money will be withdrawn when, and only when, the economy can absorb it.” That is the Taylor Rule applied to a different instrument. The Fed’s existing dual mandate already defines the observable indicators for monetary policy. Congress would need to authorize the instruments and codify the monetary financing framework; the operational mechanics already exist.

What the Public Accounts Would Show

The current system does not merely conceal the existence of monetary financing. It systematically distorts the public accounts in ways that make the fiscal situation appear worse than it is, and that distortion is used reliably to justify austerity measures whose necessity is partly an artifact of the accounting.

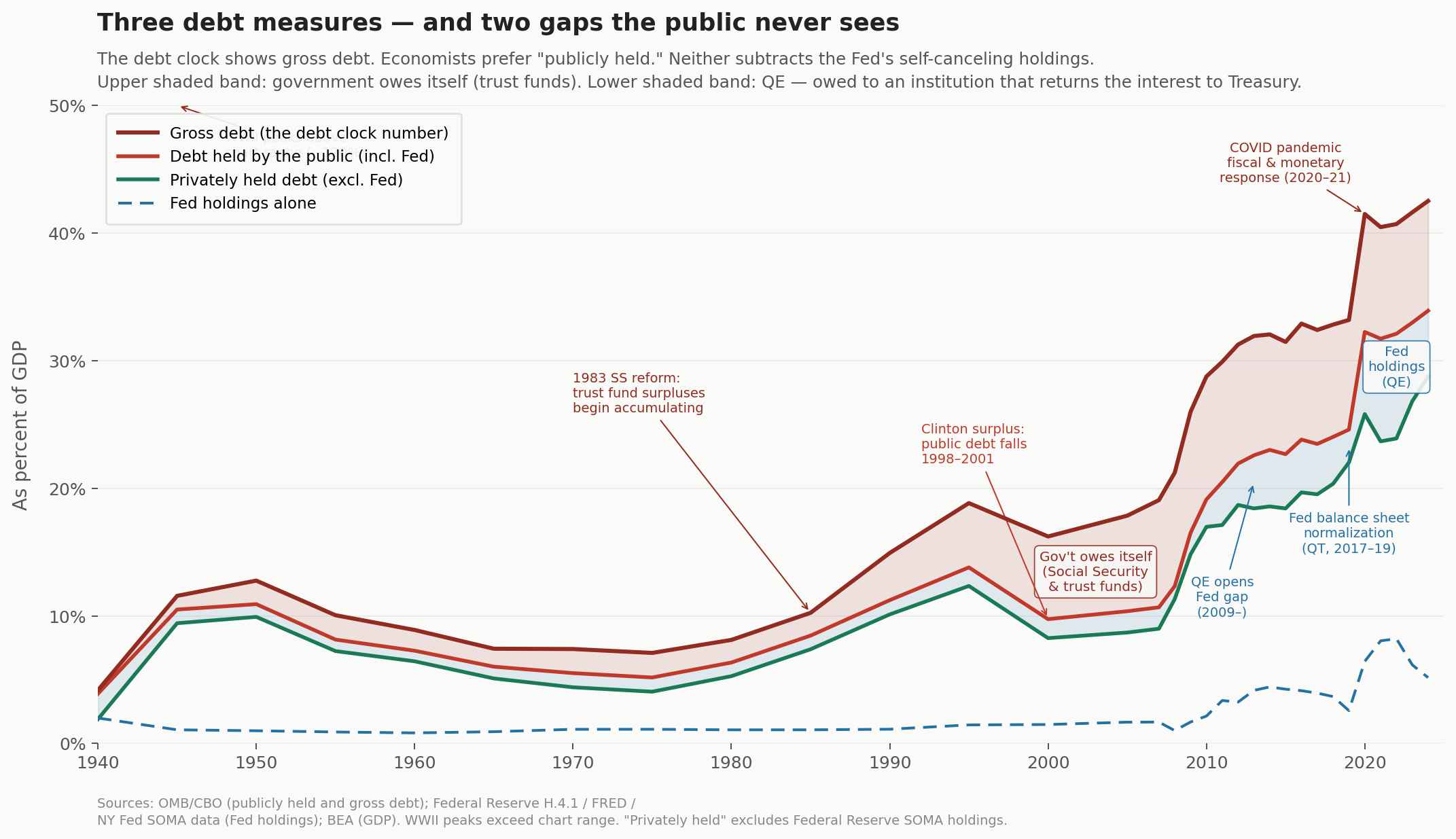

Every discussion of the national debt distinguishes between “gross debt” and “debt held by the public.” Gross debt is approximately $39 trillion. Debt held by the public is approximately $30 trillion. The difference — roughly $7 trillion — is intragovernmental debt, primarily the Social Security Trust Fund IOUs examined in the first essay of this series: accounting entries representing one government account’s claim on another, not genuine obligations to external creditors.

But “debt held by the public” includes the Federal Reserve. The Fed’s Treasury holdings — approximately $4.3 trillion — are counted as public debt alongside holdings by pension funds, foreign governments, and individual investors. A pension fund that holds Treasury bonds has a genuine claim on future tax revenues. The Federal Reserve holds Treasury bonds and collects interest on them, but returns most of that interest to the Treasury. The Fed is not a creditor in any economically meaningful sense. It is a government institution holding an obligation that generates a payment flowing back to the obligor.

The Fed is included in “debt held by the public” because the Federal Reserve banks are technically private corporations — chartered by Congress and owned by member banks, but not federal government agencies in the strict legal sense. Treasury’s definition of “held by the public” means held outside federal government accounts, and the Fed falls outside that boundary by legal classification. The terminology reflects a legal fact. It does not reflect an economic fact.

For much of the Fed’s history, before 2008, the Fed’s stock of Treasury securities was modest enough that including or excluding it in “debt held by the public” made little practical difference. Before QE, the Fed holdings were only about $700 billion, but after four rounds of QE, they expanded to $9 trillion at peak. The gap between “publicly held” and “privately held” — debt owed to genuine external creditors — is now measurable in trillions. The chart accompanying this essay shows four lines: gross debt, debt held by the public including the Fed, privately held debt excluding the Fed, and the Fed’s holdings alone.¹⁰ Before 2008, the publicly-held and privately-held lines are nearly indistinguishable. After 2008, they diverge, and the divergence tells the story of QE more accurately than any official description of those programs does.

Treasury’s own advisory body understands this. The Treasury Borrowing Advisory Committee noted in its February 2026 letter to the Secretary that Treasury securities in the Fed’s SOMA portfolio are “offsetting liabilities of the Treasury and assets of the Fed,” so that “the liability side of the consolidated balance sheet consists of only those Treasury securities which are privately held.”⁸ The government’s own senior fiscal advisors use the consolidated balance sheet framework internally, treating Fed-held debt as self-canceling, while the public debate focuses on gross figures that include it as genuine external obligation. The Federal Reserve Bank of Dallas publishes a FRED data series — MVPHGFD027MNFRBDAL — tracking the market value of privately held gross federal debt, excluding Fed holdings.⁹ It is available to anyone. It is cited by no one in the public debate.

The gap between the standard public accounts and an honest accounting produces two specific distortions.

The first is in the debt level. The headline figure — gross debt, approximately $39 trillion — includes intragovernmental holdings ($7 trillion, primarily trust funds representing the government owing money to itself) and Fed holdings ($4.3 trillion, debt owed to an institution that remits most of its earnings to Treasury). The genuinely external debt, owed to pension funds, foreign governments, individual investors, and financial institutions with real claims on future tax revenues, is closer to $26 trillion. This is still a large number. But it is meaningfully different from $39 trillion, and the difference matters when politicians and commentators argue that the debt level is at or near a crisis threshold.

The second distortion is in the interest burden. Federal interest payments are currently reported at roughly $900 billion annually — among the largest line items in the federal budget and the figure most frequently cited in arguments for fiscal consolidation. This figure includes interest paid to the Fed, which in normal times is returned to Treasury through remittances. The net interest cost — what the government actually pays to genuine external creditors — is substantially lower. During 2022 to 2025, when the Fed raised rates to combat inflation, its interest costs on bank reserves exceeded its earnings on the fixed-coupon bonds acquired during QE, creating an operating loss that suspended remittances entirely; Treasury was left paying full coupon rates on Fed-held debt with no offsetting return. Throughout this period the Fed continued meeting its obligations by crediting reserve accounts — a monetary sovereign proxy cannot be insolvent in the currency it manages — while recording the shortfall as a deferred asset to be recovered from future earnings. The deferred asset is an accounting entry, not a crisis. But it reveals the structural vulnerability of the covert system: the apparent zero-cost of Fed-financed debt holds only when monetary policy is accommodative.¹¹

Zero-interest instruments would eliminate this vulnerability entirely. A consol pays no coupon; there is no remittance mechanism to break down. The financing cost is genuinely zero in all rate environments, not contingently zero when the Fed happens to be making money. Worth noting in passing: the remittances themselves function economically less like an investment return than like a levy on private income streams — the government capturing a share of interest flows it inserted itself into by creating money, not by contributing real capital. The full implications of that observation belong to a later discussion of taxation and what a return on government co-investment actually means.¹²

When transparent instruments replace the current covert system, the monetary financing stock would be classified as government self-financing and removed from the external debt figures. Citizens evaluating fiscal policy would see an external debt several trillion dollars lower than the headline figure and an interest burden hundreds of billions of dollars lower than the gross figure. They do not have this now.

The Question That Cannot Currently Be Asked

Every year, Congress makes an implicit decision about how much of government spending will be financed by taxation, how much by borrowing from the public, and how much by monetary financing. The first two components are debated, reported, scored by the CBO, and subjected to democratic scrutiny. The third is left to the Federal Reserve under the label of monetary policy and never acknowledged as a fiscal decision at all.

“How much should be monetized and how much borrowed in any given year?” cannot be asked in any public forum, because one side of it — the monetization option — is officially nonexistent.

Serious economists and institutions have arrived at four distinct positions on the desirable quantity of monetary financing, none of which has penetrated public debate. The AIER and the fiscal conservative establishment hold that the answer is always zero — any positive amount of monetary financing leads inevitably to Weimar or Zimbabwe. They ignore conditionality, treat the worst available historical examples as universal, and decline to engage with the empirical record of quantitative easing which conducted monetary financing at $5 trillion scale without producing hyperinflation. The IMF, in its 2022 research paper, holds that the answer depends on conditions — strong central bank independence, low initial inflation, and manageable fiscal deficits make some amount of monetary financing safe; their absence makes it dangerous — but articulates this as a technical judgment for expert institutions rather than a question for democratic deliberation.³ Sheard and mainstream financial analysis hold that the answer depends on whether the operation is permanent or reversible and on the quality of the institutional framework — right as far as it goes, still a technical judgment.⁴ Turner, speaking at the IMF’s own conference in 2015, holds that the technical case is settled and the real questions are political — this is the most honest framing available — yet even Turner does not acknowledge that the debate is being conducted in the abstract while the practice occurs covertly at massive scale under a different name.⁵

None of these four positions asks who should make this decision, or whether the public should know it is being made. Making transparent monetary financing legal — not unlimited, not ungoverned, but explicit, subject to observable rules, and reported in the public accounts — would not settle the question of how much monetization is appropriate. It would make the question askable. That is democratic deliberation, and it is what is currently impossible.

Who Are We Fooling?

The invisibility of monetary financing is not primarily about hiding the truth from the public, though that is a consequence. It is about managing what Congress believes it can and cannot do.

The Federal Reserve’s institutional independence depends, in part, on Congress not asking why fiscal decisions are being made by an unelected committee under monetary policy cover. QE is fiscal policy. It decides how much of Treasury’s deficit spending is financed by money creation rather than by genuine public borrowing. That decision has distributional consequences — it affects asset prices, credit conditions, the real value of savings, and the cost of the government’s debt. It is made by twelve voting members of the Federal Open Market Committee, none elected, none describing what they are doing as fiscal policy. Sheard himself acknowledged that QE combined with large fiscal deficits “is probably best viewed as a monetary operation of the consolidated government” — a fiscal decision.⁴ The institutional framing prevents that characterization from becoming politically actionable.

The economics profession has a related interest. Economists who understand fiat currency and monetary operations routinely defer to commodity-currency language in public, in congressional testimony, and in op-eds, because that is the vocabulary their audiences recognize and because departing from it carries professional and political costs. The cumulative effect is a sustained public education in a framework that has been inaccurate since at least 1971. Each individual accommodation seems reasonable. The aggregate is systematic, and the public debates fiscal policy inside a frame that excludes one of the options on the menu.

The fiscal conservative policy community has a straightforwardly political interest in maintaining the fiction. “We can’t afford it” sounds like a statement of fact rather than a statement of values, it preempts deliberation about priorities, and it forecloses the question of who bears the cost of the things we allegedly cannot afford. If the existence of a third fiscal option were public knowledge, “we can’t afford it” would have to be replaced with “we have chosen not to finance it this way” — a statement that requires justification and invites scrutiny. Maintaining the fiction converts a political position into an apparent statement of natural law.

The primary dealer community’s interest is direct and measurable. The Fed’s open-market requirement generates billions of dollars annually in dealer spreads that would not exist if Treasury could deal directly with the Fed.¹⁴ Whether the requirement was originally inserted at dealer request, as Eccles believed, is historical interpretation. That it currently generates substantial private profit from a public operation is undeniable.

None of these actors needs to coordinate. Each operates within professional norms and institutional incentives that happen to point in the same direction. The result is a public debate conducted on the premise that a third fiscal option does not exist, even though that option is exercised at multi-trillion dollar scale by institutions that have every reason to call it something else.

Article I, Section 8 assigns to Congress the power to borrow money on the credit of the United States. The current system effectively transfers a portion of a closely related authority — the authority to decide how much of the government’s deficit spending is financed by money creation — to the Federal Reserve, by maintaining a fiction that prevents Congress from knowing the authority exists. Whether the Fed makes better decisions than Congress is a separate question. The question here is who is constitutionally empowered to make the decision, and whether democratic institutions can exercise authority they don’t know they have.

Who Benefits From Congressional Ignorance?

The actors identified above share a specific interest that unifies them despite their different institutional positions: they all benefit from Congress not knowing that a third fiscal instrument exists and is already being used.

The argument for maintaining congressional ignorance — made explicitly or implicitly — is that Congress cannot be trusted with the truth. Democratic institutions given access to zero-cost financing will use it irresponsibly. Political incentives systematically favor spending over fiscal discipline. The inflation risk is real and democratic institutions are poorly equipped to resist it.

This argument has genuine force. The historical record of democratic governments with direct access to monetary financing includes real inflationary disasters. The political economy logic is sound. The concern is not paranoid.

But the argument concedes something its proponents do not acknowledge. It is not an argument that monetary financing is always wrong. It is an argument that democratic institutions cannot be trusted to govern it. This raises a question: if democratic institutions cannot be trusted with transparent monetary financing, why can they be trusted with covert monetary financing? The current system does not prevent monetary financing. It prevents congressional oversight of monetary financing. The Fed makes the decision. Congress is excluded from it. The justification is democratic incapacity; the result is rule by technocracy under cover of a fiction about legal prohibition.

The people who benefit from congressional ignorance are the same people invoking congressional irresponsibility as the justification for that ignorance. “They can’t handle the truth” is the argument made by those who profit from their not knowing it.

Can We Trust Congress With the Truth?

The political discipline objection deserves full engagement. The IMF’s empirical findings confirm that monetary financing produces modest inflation effects under conditions of strong central bank independence and low initial inflation — and much stronger effects when those conditions are absent.³ The historical record includes genuine inflationary disasters. These are serious arguments, grounded in real experience.

The conditional-rule framework developed above answers them without dismissing them. The credibility-commitment problem dissolves when the right question replaces the wrong one. Can the government make a credible commitment to permanent non-reversal? That question has no satisfying answer. Can the government make a credible commitment that reversal will occur only when economic conditions make it benign? That question does, because central banks make exactly this kind of conditional commitment routinely — it is called forward guidance, and markets find it credible.

The accountability argument is equally important. A Congress that knows it is making a monetary financing decision, and knows the public knows, faces different incentives than a Fed committee making the same decision under cover of monetary policy language. Accountability changes behavior. A politician who votes for monetary financing that subsequently generates inflation faces that record. A Fed committee that expands the balance sheet through QE faces no comparable accountability, because the monetary policy framing insulates the fiscal decision from democratic review.

Covert monetary financing — the system we have — operates without a published rule, a public ledger, democratic accountability, or political cost for excess. Transparent monetary financing, governed by a publicly stated conditional rule tied to observable economic indicators, has all of these. The covert system does not protect against irresponsibility. It protects against scrutiny.

Stripped of its technical language, the political discipline argument makes a specific claim: that the public and their elected representatives cannot be trusted with an accurate understanding of how their government finances itself. The entire apparatus — the statutory prohibitions, the institutional conventions, the careful language of open market operations and quantitative easing — exists to maintain that position.

The case for the current system, stated honestly, is that Congress and the public cannot be trusted with an accurate account of their government’s fiscal options. The technical apparatus — the statutory prohibitions, the institutional conventions, the careful language of monetary policy — exists to maintain that position. So does the precedent. And so do the financial interests of those who collect a toll every time the government does, covertly, what the law says it cannot do at all.

“You want the truth? You can’t handle the truth!” — Col. Nathan Jessup, A Few Good Men (1992)

Notes

The statutory architecture relevant to money creation: Federal Reserve Act §14, codified at 12 U.S.C. §355 (direct purchase prohibition, enacted 1935; wartime exemption lapsed June 1, 1981); Second Liberty Bond Act of 1917, consolidated into the Public Debt Acts of 1939 and 1941, now at 31 U.S.C. §3101 (debt ceiling); U.S. Constitution, Art. I, §9, cl. 7 (Appropriations Clause). The Emergency Banking Act of 1933 explicitly authorized direct Fed purchases of Treasury securities; the Banking Act of 1935 reversed this without stated rationale. The Legal Tender Act of 1862, 12 Stat. 345, authorized the original issuance of United States Notes (Greenbacks), enabling the Civil War government to create money through physical currency delivered directly to payees; final issuance of that series concluded in 1971. Congress permanently repealed the Treasury’s note-reissuance requirements in 1994, Pub. L. 103–325, title VI, §602(f)(4)(B). Treasury’s authority to maintain its own depositary functions is recognized in 31 U.S.C. §3322, but in practice no modern counterparty accepts Treasury instruments unless they clear through the Federal Reserve system. The Antideficiency Act, 31 U.S.C. §1341, constrains spending authority rather than money creation and is discussed in the debt ceiling essay.

The 1935 prohibition and its contested rationale: Kenneth D. Garbade, “Direct Purchases of U.S. Treasury Securities by Federal Reserve Banks,” Federal Reserve Bank of New York Liberty Street Economics, September 29, 2014. https://libertystreeteconomics.newyorkfed.org/2014/09/direct-purchases-of-us-treasury-securities-by-federal-reserve-banks/. The three competing explanations — Eccles on dealer lobbying, Burgess on balance sheet limits, others on deficit deterrence — are documented in the Garbade source. The wartime exemption was authorized by the Second War Powers Act of 1942, which framed it explicitly as restoring a cash management safety net; Congress chose a $5 billion cap rather than full repeal even under wartime emergency, a pattern consistent with the dealer-protection explanation for the original prohibition. In 1977 and 1979, Treasury used the remaining direct purchase authority as a bridge during debt ceiling impasses — providing speed and market-independence rather than additional fiscal capacity, since direct purchases counted against the ceiling the same as open market sales. Representative Ron Paul’s characterization of those uses as an “end run around Congress” was constitutionally confused: Treasury was honoring spending Congress had already appropriated, accessing headroom that existed under the ceiling, doing so faster than market methods would allow. The political toxicity of the ceiling-bridge use, combined with the practical obsolescence of the authority after cash management bills were introduced in 1975, made renewal impossible in 1981.

IMF (2022): Itai Agur, Damien Capelle, Giovanni Dell’Ariccia, and Damiano Sandri, “Monetary Finance: Do Not Touch, or Handle with Care?” IMF Departmental Paper DP/2022/001, January 2022. https://www.elibrary.imf.org/view/journals/087/2022/001/article-A001-en.xml.

Sheard (2014): Paul Sheard, “A QE Q&A: Everything You Ever Wanted to Know About Quantitative Easing,” S&P Economic Research / Harvard Kennedy School, August 7, 2014. https://www.hks.harvard.edu/sites/default/files/centers/mrcbg/files/PSheardQEQAAugust2014.pdf.

Turner (2015): Adair Turner, “The Case for Monetary Finance — An Essentially Political Issue,” IMF Jacques Polak Annual Research Conference, November 5–6, 2015. https://www.imf.org/external/np/res/seminars/2015/arc/pdf/adair.pdf.

The primary dealer system: the Federal Reserve Bank of New York maintains the current list of designated primary dealers and their obligations. As of 2026, approximately 25 dealers are designated. Unlike other auction participants — including foreign central banks, pension funds, and asset managers who may bid directly — primary dealers are obligated to participate in every Treasury auction at competitive prices. More importantly for the monetary financing circuit, they are the exclusive counterparties for Federal Reserve open market operations; the Fed buys only from primary dealers, not from the broader universe of auction participants. The open-market requirement that makes dealer intermediation mandatory in the Fed purchasing channel is 12 U.S.C. §355.

Functional Finance: Abba P. Lerner, “Functional Finance and the Federal Debt,” Social Research, Vol. 10, No. 1 (February 1943), pp. 38–51. Lerner’s capacity-constraint formulation: fiscal policy should be adjusted “only insofar as this is needed for the purpose of keeping the rate of spending neither too low (so as to cause unemployment) nor too high (so as to cause inflation).” The Weimar and Zimbabwe hyperinflations are consistent with this framework: both occurred in economies that had lost productive capacity, making additional money creation inflationary regardless of the financing instrument used. The United States during QE1–QE3 had the opposite conditions: substantial slack, high unemployment, and deflationary pressure, producing the below-target inflation the framework predicts. The 2021–2023 inflation episode was primarily driven by pandemic-era fiscal transfers directly to households — bypassing bank intermediation and hitting goods markets directly — combined with supply chain disruption and energy price shocks, rather than by the QE reserves that had accumulated since 2009.

TBAC consolidated balance sheet framework: Treasury Borrowing Advisory Committee, Report to the Secretary of the Treasury, February 3, 2026. https://home.treasury.gov/news/press-releases/sb0385. The quoted language on SOMA holdings as “offsetting liabilities” appears in the discussion of privately held marketable borrowing.

Dallas Fed FRED series: Federal Reserve Bank of Dallas, “Market Value of Privately Held Gross Federal Debt,” FRED series MVPHGFD027MNFRBDAL. https://fred.stlouisfed.org/series/MVPHGFD027MNFRBDAL. Monthly data from January 1942.

FRED Blog decomposition: Federal Reserve Bank of St. Louis, “Who Holds US National Debt?” FRED Blog, March 6, 2025. https://fredblog.stlouisfed.org/2025/03/who-holds-us-national-debt/. The chart referenced in this essay shows four series as percent of GDP: gross federal debt, debt held by the public including the Federal Reserve, privately held debt excluding the Federal Reserve, and Fed holdings alone. The lower shaded band — the gap between publicly held and privately held — represents the Fed’s Treasury holdings: debt the government owes to an institution that remits most of its earnings back to Treasury. Before 2008 this band was negligible. After four rounds of QE it widened to several percentage points of GDP, narrowed during the quantitative tightening of 2017–2019, exploded during QE4, and has been narrowing again since 2022.

The Fed’s operating losses, suspended remittances, and deferred asset: when the Fed raises rates, it pays higher interest on the reserve balances that commercial banks hold at the Fed than it earns on the fixed-coupon bonds acquired during earlier QE rounds. Operating losses from late 2022 onward were recorded as a “deferred asset” — a bookkeeping entry representing future earnings needed before remittances resume, not a solvency event. The Fed continued meeting all obligations throughout by crediting reserve accounts. The deferred asset reached over $130 billion by mid-2024. Under consolidated accounting, the interest the Fed pays on bank reserves during such periods would appear in the federal budget as a transfer payment to the financial sector — a subsidy that in 2022–2025 exceeded $100 billion annually while appearing nowhere in the public accounts.

The remittances-as-levy observation: in Functional Finance terms, Fed remittances to Treasury function economically less like an investment return and more like a levy on private income streams — the government capturing a share of interest flows it inserted itself into by creating money, not by contributing real capital. The Cary Brown theorem, which shows that under full expensing the corporate tax becomes the government collecting its equity return on contributed capital, illuminates the contrast: Cary Brown involves a real contribution earning a real return; monetary financing involves a costless creation earning what is structurally a levy. The full implications of this parallel belong to the later essays on taxation and what a return on government co-investment actually means.

Gold revaluation as another hidden fiscal option. The United States holds approximately 261.5 million fine troy ounces of gold, nearly all of it monetized: gold certificates issued to the Federal Reserve equal the statutory value of the gold stock, currently $11.037 billion against a statutory value of $11.041 billion (the $4 million gap is a 100,000-troy-oz buffer set aside in 2002 as a bookkeeping safeguard). Per 31 U.S.C. §§5116–5117, the statutory price has been frozen at $42.2222 per troy ounce since 1973. At the market price of approximately $3,300 per ounce in 2025, the gold stock’s market value is roughly $863 billion — a latent fiscal capacity of approximately $852 billion accessible in principle through a statutory revaluation. This is not without precedent: the Gold Reserve Act of 1934 raised the statutory price from $20.67 to $35 per ounce, generating a windfall TGA credit used to capitalize the Exchange Stabilization Fund. In real (2025) dollar terms, the 1934 statutory price of $35 was equivalent to approximately $833 per ounce today; the 1980 market peak of $615 nominal was approximately $2,381 in 2025 dollars — substantial, but still below today’s market price of approximately $3,300. With holdings quantities nearly unchanged since 1980, the current total real market value of US gold holdings of approximately $863 billion is a genuine real as well as nominal all-time high. The current statutory price of $42.22, frozen for fifty-two years, represents less than 1.3% of the market price — a gap that grows larger in real terms with every year of inflation. The economic objections to revaluation today are substantially weaker than in 1934, because the dollar is no longer convertible to gold; a revaluation would be a pure accounting adjustment with no direct effect on exchange rates or the monetary system. The objections are primarily political: that it would make visible a large fiscal resource that “we can’t afford it” rhetoric requires to be invisible, and that it would blur the institutional line between monetary and fiscal operations that central bank independence doctrine requires to appear sharp. Congressional Research Service, “The Federal U.S. Gold Stock,” IF13109, September 23, 2025, https://www.congress.gov/crs-product/IF13109; Federal Reserve, “Does the Federal Reserve Own or Hold Gold?” https://www.federalreserve.gov/faqs/does-the-federal-reserve-own-or-hold-gold.htm.

Dealer revenue from Treasury market-making during QE periods is estimated at billions of dollars annually based on transaction volumes and typical spread ranges, but precise figures are not publicly reported as a separate line item in dealer financial statements. The Federal Reserve Bank of New York publishes dealer position data (FR 2004 reports) but not profit and loss by activity. The estimate follows from monthly Fed purchase volumes of $80–120 billion multiplied by typical round-trip spreads across auction and secondary market legs. This is an informed estimate grounded in published volume data rather than a verified figure.